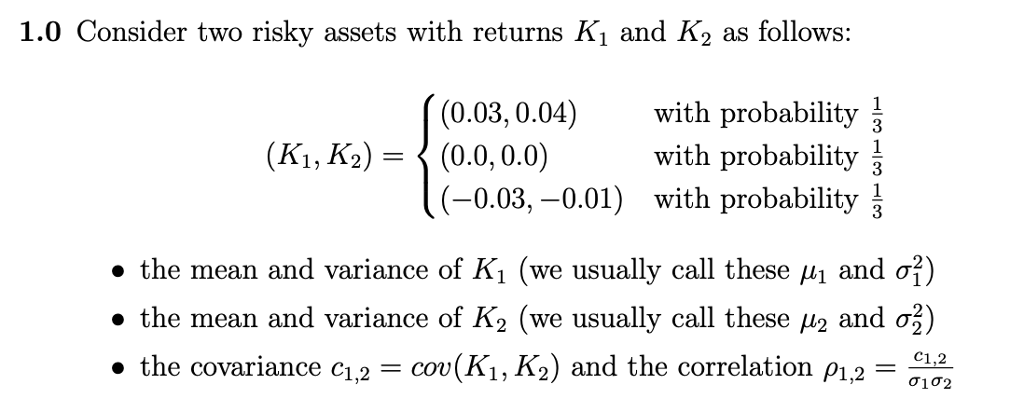

Question: 1.0 Consider two risky assets with returns Ki and K2 as follows (0.03,0.04) with probability with probability (-0.03,-0.01) with probability (Ki, K2)- (0.0,0.0) . the

1.0 Consider two risky assets with returns Ki and K2 as follows (0.03,0.04) with probability with probability (-0.03,-0.01) with probability (Ki, K2)- (0.0,0.0) . the mean and variance of K (we usually call these | and ) . the mean and variance of K2 (we usually call these 2 and ) . the covariance c,-cou(K1, K2) and the correlation P1,-1,2 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock