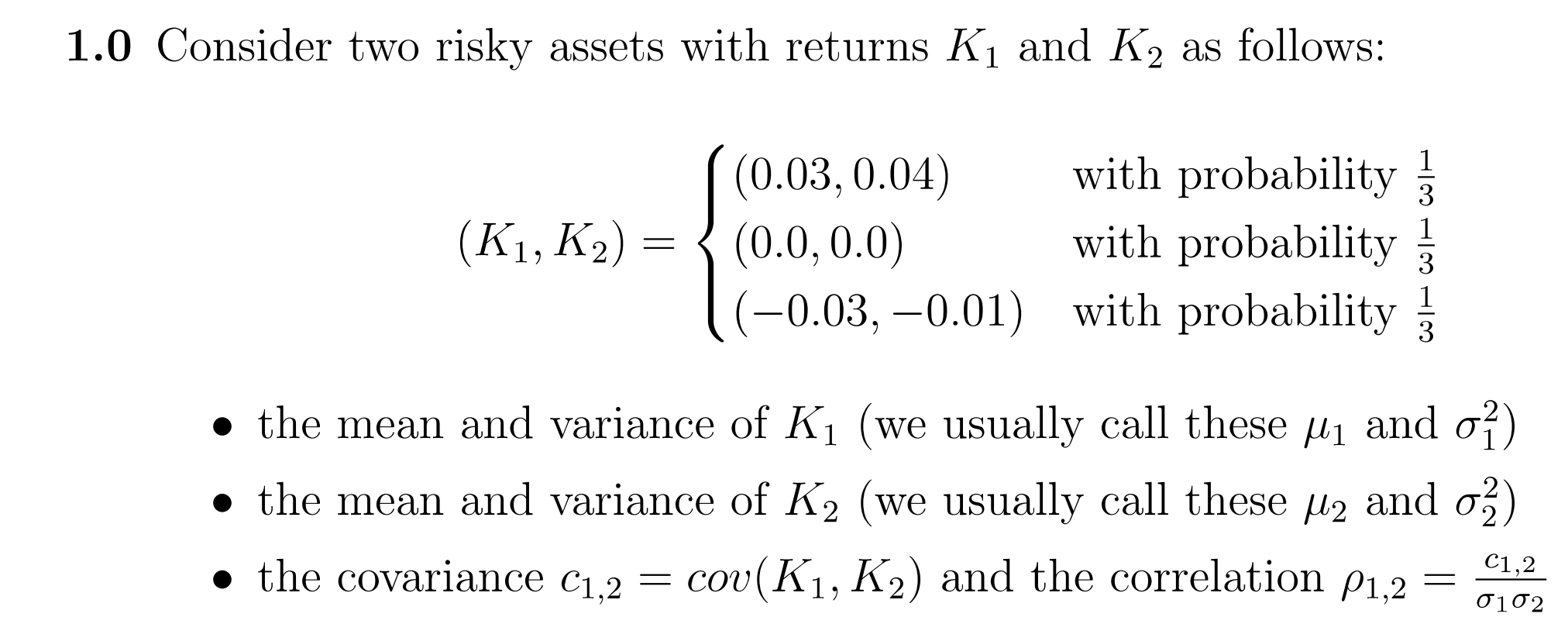

Question: 1.0 Consider two risky assets with returns K and K2 as follows: (K1, K2) = (0.03, 0.04) with probability (0.0, 0.0) with probability -0.03, -0.01)

1.0 Consider two risky assets with returns K and K2 as follows: (K1, K2) = (0.03, 0.04) with probability (0.0, 0.0) with probability -0.03, -0.01) with probability the mean and variance of Ki (we usually call these Mi and o) the mean and variance of K2 (we usually call these M2 and o) the covariance C1,2 COU(K1, K2) and the correlation P1,2 = C1,2 0102

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock