Question: (10 points). 2. You are given the following data. All forward rates are expected future six-month rates. All rates are stated annually, as BEYs. If

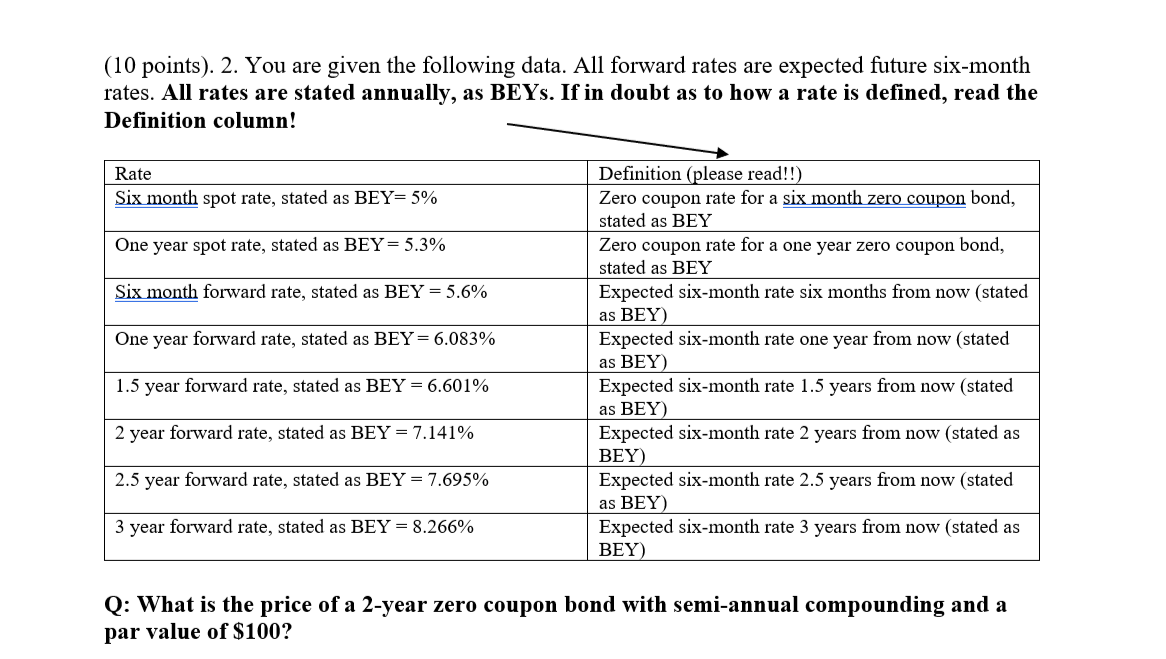

(10 points). 2. You are given the following data. All forward rates are expected future six-month rates. All rates are stated annually, as BEYs. If in doubt as to how a rate is defined, read the Definition column! Rate Six month spot rate, stated as BEY= 5% One year spot rate, stated as BEY= 5.3% Six month forward rate, stated as BEY = 5.6% One year forward rate, stated as BEY=6.083% Definition (please read!!) Zero coupon rate for a six month zero coupon bond, stated as BEY Zero coupon rate for a one year zero coupon bond, stated as BEY Expected six-month rate six months from now (stated as BEY) Expected six-month rate one year from now (stated as BEY) Expected six-month rate 1.5 years from now (stated as BEY) Expected six-month rate 2 years from now (stated as BEY) Expected six-month rate 2.5 years from now (stated as BEY) Expected six-month rate 3 years from now (stated as BEY) 1.5 year forward rate, stated as BEY = 6.601% 2 year forward rate, stated as BEY = 7.141% 2.5 year forward rate, stated as BEY = 7.695% 3 year forward rate, stated as BEY = 8.266% Q: What is the price of a 2-year zero coupon bond with semi-annual compounding and a par value of $100? (10 points). 2. You are given the following data. All forward rates are expected future six-month rates. All rates are stated annually, as BEYs. If in doubt as to how a rate is defined, read the Definition column! Rate Six month spot rate, stated as BEY= 5% One year spot rate, stated as BEY= 5.3% Six month forward rate, stated as BEY = 5.6% One year forward rate, stated as BEY=6.083% Definition (please read!!) Zero coupon rate for a six month zero coupon bond, stated as BEY Zero coupon rate for a one year zero coupon bond, stated as BEY Expected six-month rate six months from now (stated as BEY) Expected six-month rate one year from now (stated as BEY) Expected six-month rate 1.5 years from now (stated as BEY) Expected six-month rate 2 years from now (stated as BEY) Expected six-month rate 2.5 years from now (stated as BEY) Expected six-month rate 3 years from now (stated as BEY) 1.5 year forward rate, stated as BEY = 6.601% 2 year forward rate, stated as BEY = 7.141% 2.5 year forward rate, stated as BEY = 7.695% 3 year forward rate, stated as BEY = 8.266% Q: What is the price of a 2-year zero coupon bond with semi-annual compounding and a par value of $100

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts