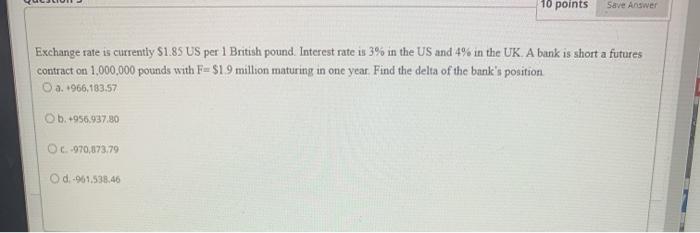

Question: 10 points Save Answer Exchange rate is currently $1.85 US per 1 British pound. Interest rate is 3% in the US and 4% in the

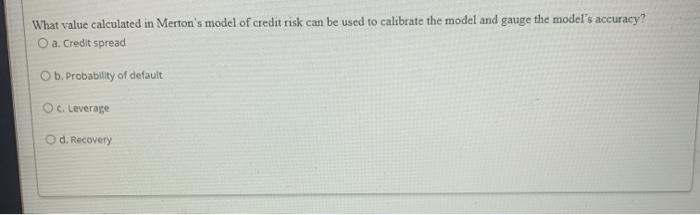

10 points Save Answer Exchange rate is currently $1.85 US per 1 British pound. Interest rate is 3% in the US and 4% in the UK. A bank is short a futures contract on 1,000,000 pounds with F= $19 million maturing in one year. Find the delta of the bank's position, a. 1966,183.57 Ob. 1956.937.80 OC.-970,873.79 Od..961.538.46 What value calculated in Merton's model of credit risk can be used to calibrate the model and gauge the model's accuracy? O a. Credit spread O b. Probability of default OC. Leverage Od: Recovery

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock