Question: 11. Mike has a utility function U(W)=W02, and his initial wealth is $10,000. Mike feels that he faces the following probability distributions of losses with

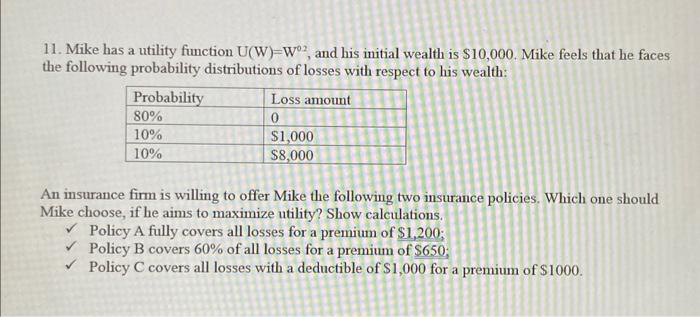

11. Mike has a utility function U(W)=W02, and his initial wealth is $10,000. Mike feels that he faces the following probability distributions of losses with respect to his wealth: Probability Loss amount 80% 0 10% $1,000 10% $8,000 An insurance firm is willing to offer Mike the following two insurance policies. Which one should Mike choose, if he aims to maximize utility? Show calculations Policy A fully covers all losses for a premium of $1,200; Policy B covers 60% of all losses for a premium of $650; Policy C covers all losses with a deductible of $1,000 for a premium of $1000

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock