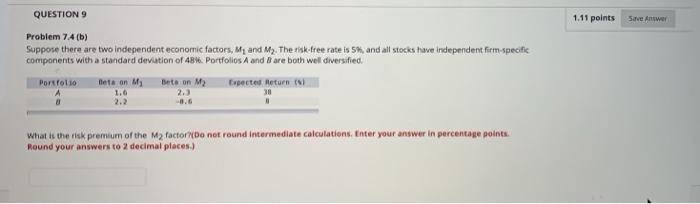

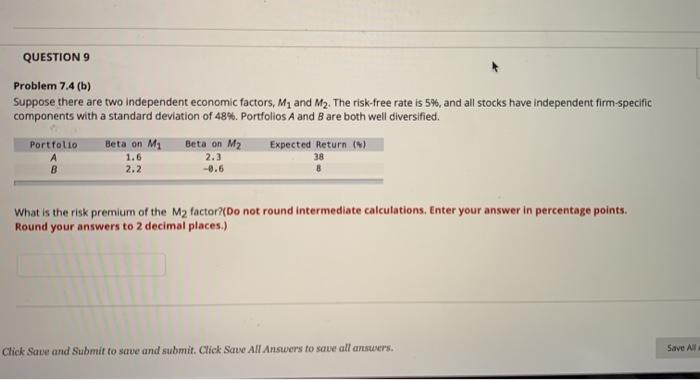

Question: 1.11 points Save Answer QUESTION 9 Problem 74 (b) Suppose there are two independent economic factors, My and M2. The risk free rate is 5%,

1.11 points Save Answer QUESTION 9 Problem 74 (b) Suppose there are two independent economic factors, My and M2. The risk free rate is 5%, and all stocks have independent firm specific components with a standard deviation of 48%. Portfolios A and B are both well diversified Portfolio eta on M Bet on My Expectes Heturn 1.6 2.) -0.6 What is the risk premium of the Ma factor do not round intermediate calculations, Inter your answer in percentage points Round your answers to 2 decimal places.) QUESTION 9 Problem 7.4(b) Suppose there are two independent economic factors, M, and M2. The risk-free rate is 5%, and all stocks have independent firm-specific components with a standard deviation of 48%. Portfolios A and B are both well diversified. Portfolio Beta on Ma Beta on M2 Expected Return (9) 38 2.2 -8.6 1.6 2.3 What is the risk premium of the M2 factor?(Do not round intermediate calculations, Enter your answer in percentage points. Round your answers to 2 decimal places.) Click Save and Submit to save and submit. Click Save All Answers to save all answers. Save A

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts