Question: (13) Consider the standard Black-Scholes framework. What is the forward price of a European claim that will pay S(T), at the terminal time T, when

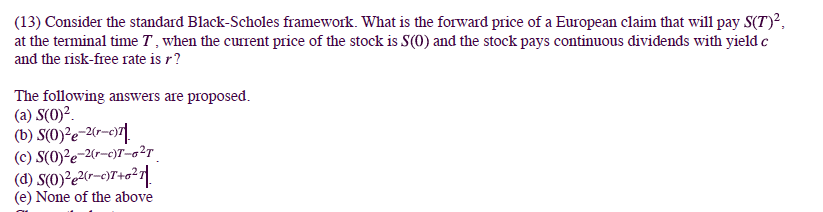

(13) Consider the standard Black-Scholes framework. What is the forward price of a European claim that will pay S(T), at the terminal time T, when the current price of the stock is S(O) and the stock pays continuous dividends with yield c and the risk-free rate is r? The following answers are proposed. (a) S(0)2 (b) S(O)2e-2- (c) S(O)2e-2r-c)T-027 (d) S(O)2e2(r-c)7+0211 (e) None of the above (13) Consider the standard Black-Scholes framework. What is the forward price of a European claim that will pay S(T), at the terminal time T, when the current price of the stock is S(O) and the stock pays continuous dividends with yield c and the risk-free rate is r? The following answers are proposed. (a) S(0)2 (b) S(O)2e-2- (c) S(O)2e-2r-c)T-027 (d) S(O)2e2(r-c)7+0211 (e) None of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts