Question: 15. (5pts) Bootstrap Given instruments in below table Instrument om (182 day) T-Bill 2y Treasury 3y Treasury 5y Treasury 7y Treasury 10y Treasury Semi-annual Market

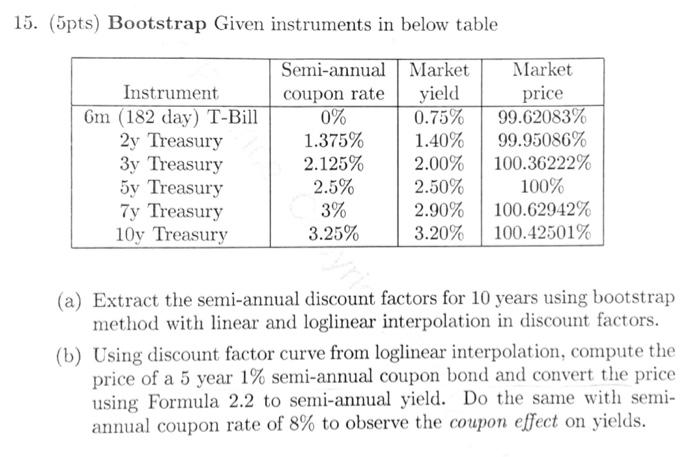

15. (5pts) Bootstrap Given instruments in below table Instrument om (182 day) T-Bill 2y Treasury 3y Treasury 5y Treasury 7y Treasury 10y Treasury Semi-annual Market coupon rate yield 0% 0.75% 1.375% 1.40% 2.125% 2.00% 2.5% 2.50% 3% 2.90% 3.25% 3.20% Market price 99.62083% 99.95086% 100.36222% 100% 100.62942% 100.42501% (a) Extract the semi-annual discount factors for 10 years using bootstrap method with linear and loglinear interpolation in discount factors. (b) Using discount factor curve from loglinear interpolation, compute the price of a 5 year 1% semi-annual coupon bond and convert the price using Formula 2.2 to semi-annual yield. Do the same with semi- annual coupon rate of 8% to observe the coupon effect on yields. 15. (5pts) Bootstrap Given instruments in below table Instrument om (182 day) T-Bill 2y Treasury 3y Treasury 5y Treasury 7y Treasury 10y Treasury Semi-annual Market coupon rate yield 0% 0.75% 1.375% 1.40% 2.125% 2.00% 2.5% 2.50% 3% 2.90% 3.25% 3.20% Market price 99.62083% 99.95086% 100.36222% 100% 100.62942% 100.42501% (a) Extract the semi-annual discount factors for 10 years using bootstrap method with linear and loglinear interpolation in discount factors. (b) Using discount factor curve from loglinear interpolation, compute the price of a 5 year 1% semi-annual coupon bond and convert the price using Formula 2.2 to semi-annual yield. Do the same with semi- annual coupon rate of 8% to observe the coupon effect on yields

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts