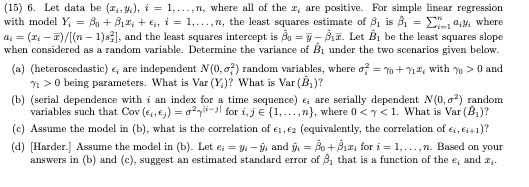

Question: (15) 6. Let data be (c,, ;), i = 1,...,n, where all of the I, are positive. For simple linear regression with model Y, =

(15) 6. Let data be (c,, ";), i = 1,...,n, where all of the I, are positive. For simple linear regression with model Y, = An + Pis, te, i = 1,..., n, the least squares estimate of 81 is A, = )" a,, where ai = (14 -F)/[(n - 1)s;], and the least squares intercept is An = 7 - 81I. Let Bj be the least squares slope when considered as a random variable. Determine the variance of Bi under the two scenarios given below. (a) (heteroscedastic) , are independent N(0, of) random variables, where of = 1% + 717, with " > 0 and > >0 being parameters. What is Var (Y,)? What is Var (B, )? (b) (serial dependence with i an index for a time sequence) e, are serially dependent N(0, o') random variables such that Cov (e , 6 ) =0 ' for i, je (1,....n}, where 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts