Question: 1.7. In the trinomial model = SU (1) = 115 A(1) = 100 S(0) = 100 A(0) = 100 -> SM (1) = 105 A(1)

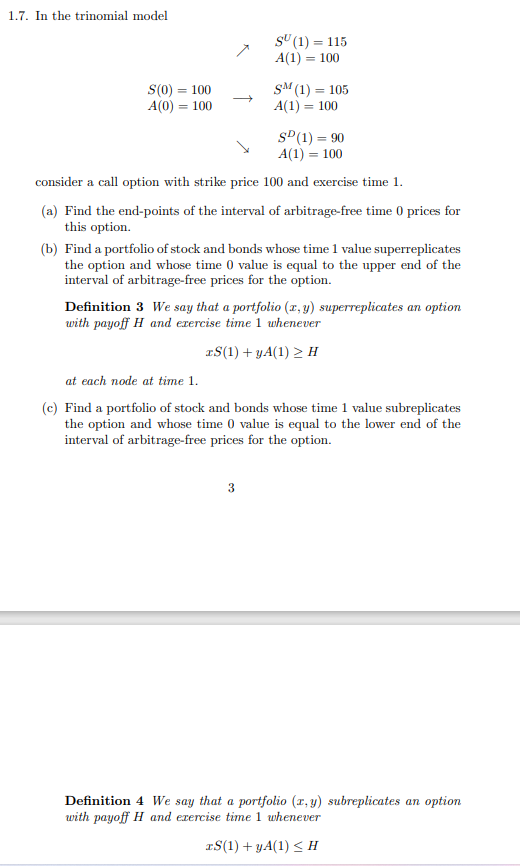

1.7. In the trinomial model = SU (1) = 115 A(1) = 100 S(0) = 100 A(0) = 100 -> SM (1) = 105 A(1) = 100 SD(1) = 90 A(1) = 100 consider a call option with strike price 100 and exercise time 1. (a) Find the end-points of the interval of arbitrage-free time 0 prices for this option. (b) Find a portfolio of stock and bonds whose time 1 value superreplicates the option and whose time 0 value is equal to the upper end of the interval of arbitrage-free prices for the option. Definition 3 We say that a portfolio I, y) superreplicates an option with payoff H and exercise time 1 whenever S(1) + yA(1) > H at each node at time 1. (c) Find a portfolio of stock and bonds whose time 1 value subreplicates the option and whose time 0 value is equal to the lower end of the interval of arbitrage-free prices for the option. Definition 4 We say that a portfolio (x,y) subreplicates an option urith payoff H and exercise time 1 whenever IS(1) +yA(1) SH 1.7. In the trinomial model = SU (1) = 115 A(1) = 100 S(0) = 100 A(0) = 100 -> SM (1) = 105 A(1) = 100 SD(1) = 90 A(1) = 100 consider a call option with strike price 100 and exercise time 1. (a) Find the end-points of the interval of arbitrage-free time 0 prices for this option. (b) Find a portfolio of stock and bonds whose time 1 value superreplicates the option and whose time 0 value is equal to the upper end of the interval of arbitrage-free prices for the option. Definition 3 We say that a portfolio I, y) superreplicates an option with payoff H and exercise time 1 whenever S(1) + yA(1) > H at each node at time 1. (c) Find a portfolio of stock and bonds whose time 1 value subreplicates the option and whose time 0 value is equal to the lower end of the interval of arbitrage-free prices for the option. Definition 4 We say that a portfolio (x,y) subreplicates an option urith payoff H and exercise time 1 whenever IS(1) +yA(1) SH

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts