Question: ( 2 0 2 1 Summer Final Q 5 3 - 5 6 ) A perfectly competitive market is initially in a long run equilibrium,

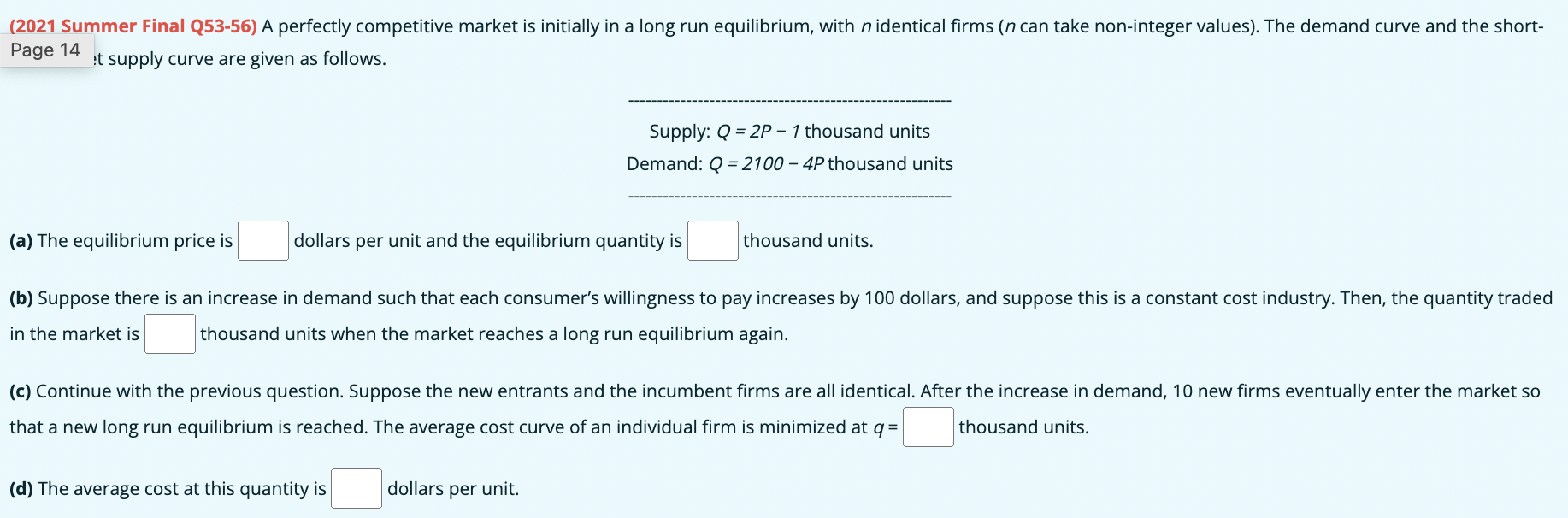

Summer Final Q A perfectly competitive market is initially in a long run equilibrium, with n identical firms n can take noninteger values The demand curve and the shortPage it supply curve are given as follows.

Supply: Q P thousand units

Demand: Q P thousand units

a The equilibrium price is dollars per unit and the equilibrium quantity is thousand units.

b Suppose there is an increase in demand such that each consumer's willingness to pay increases by dollars, and suppose this is a constant cost industry. Then, the quantity traded in the market is thousand units when the market reaches a long run equilibrium again.

c Continue with the previous question. Suppose the new entrants and the incumbent firms are all identical. After the increase in demand, new firms eventually enter the market so that a new long run equilibrium is reached. The average cost curve of an individual firm is minimized at q thousand units.

d The average cost at this quantity is dollars per unit.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock