Question: 2. (10 points) Note: This is a great opportunity to use the market conventions we dis- cussed in class. You find the quotes for

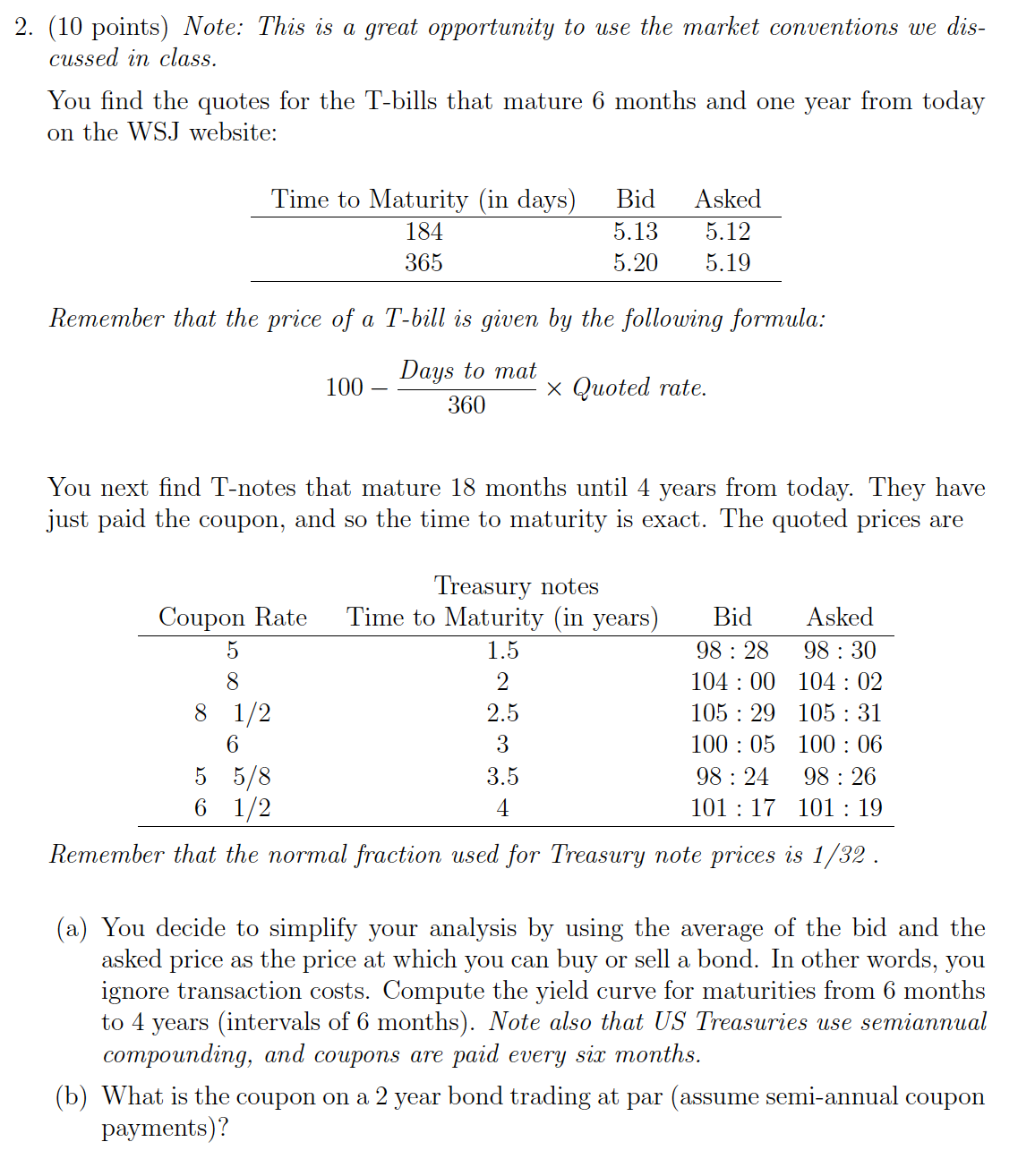

2. (10 points) Note: This is a great opportunity to use the market conventions we dis- cussed in class. You find the quotes for the T-bills that mature 6 months and one year from today on the WSJ website: Time to Maturity (in days) Bid Asked 5.13 5.12 5.20 5.19 184 365 Remember that the price of a T-bill is given by the following formula: Days to mat 100 360 Quoted rate. You next find T-notes that mature 18 months until 4 years from today. They have just paid the coupon, and so the time to maturity is exact. The quoted prices are Treasury notes Coupon Rate 5 Time to Maturity (in years) Bid Asked 1.5 98: 28 98:30 8 8 1/2 6 2 10400 104: 02 2.5 105 29 105: 31 3 10005 100: 06 5 5/8 6 1/2 3.5 9824 98: 26 4 101 17 101: 19 Remember that the normal fraction used for Treasury note prices is 1/32. (a) You decide to simplify your analysis by using the average of the bid and the asked price as the price at which you can buy or sell a bond. In other words, you ignore transaction costs. Compute the yield curve for maturities from 6 months to 4 years (intervals of 6 months). Note also that US Treasuries use semiannual compounding, and coupons are paid every six months. (b) What is the coupon on a 2 year bond trading at par (assume semi-annual coupon payments)?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts