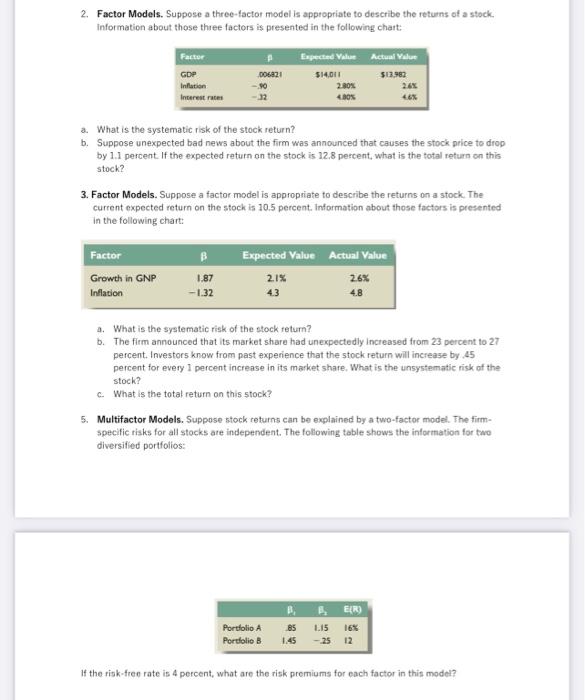

Question: 2. Factor Models. Suppose a three-factor model is appropriate to describe the returns of a stock. Information about those thee factors is presented in the

2. Factor Models. Suppose a three-factor model is appropriate to describe the returns of a stock. Information about those thee factors is presented in the following chart: a. What is the systematic risk of the stock return? b. Suppose unexpected bad news about the firm was announced that causes the stock price to drop by 1.1 percent If the expected return on the stock is 12.8 percent, what is the total return on this stock? 3. Factor Models. Suppose a factor model is appropriate to describe the returns on a stock. The current expected return on the stock is 10.5 percent. Information about those factors is presented in the following chart: a. What is the systematic risk of the stock retum? b. The firm announced that its market share had unexpectedly increased from 23 percent to 27 percent. Investors know from past experience that the stock return will increase by . 45 percent for every 1 percent increase in its market share, What is the unsystematic risk of the stock? c. What is the total return on this stock? 5. Multifactor Models. Suppose stock returns can be explained by a two-factor model. The firmspecific risks for all stocks are independent. The following table shows the information for two diversified portfolios: If the risk-free rate is 4 percent, what are the risk premiums for each factor in this model? 2. Factor Models. Suppose a three-factor model is appropriate to describe the returns of a stock. Information about those thee factors is presented in the following chart: a. What is the systematic risk of the stock return? b. Suppose unexpected bad news about the firm was announced that causes the stock price to drop by 1.1 percent If the expected return on the stock is 12.8 percent, what is the total return on this stock? 3. Factor Models. Suppose a factor model is appropriate to describe the returns on a stock. The current expected return on the stock is 10.5 percent. Information about those factors is presented in the following chart: a. What is the systematic risk of the stock retum? b. The firm announced that its market share had unexpectedly increased from 23 percent to 27 percent. Investors know from past experience that the stock return will increase by . 45 percent for every 1 percent increase in its market share, What is the unsystematic risk of the stock? c. What is the total return on this stock? 5. Multifactor Models. Suppose stock returns can be explained by a two-factor model. The firmspecific risks for all stocks are independent. The following table shows the information for two diversified portfolios: If the risk-free rate is 4 percent, what are the risk premiums for each factor in this model

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts