Question: 2. Given information below, compute the values of (a) - (h) for bonds A & B Annual coupon rate (annual frequency) | 8% EAY |

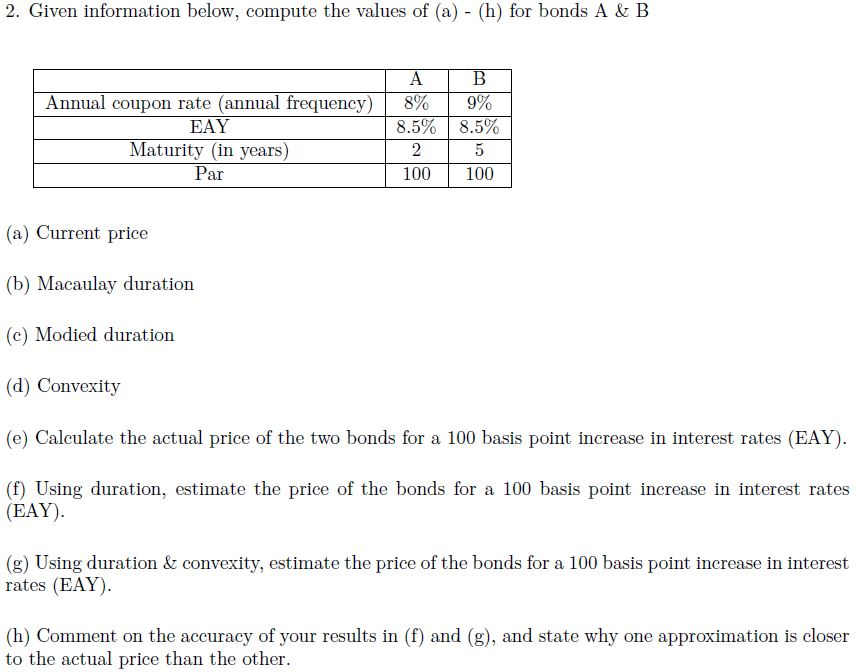

2. Given information below, compute the values of (a) - (h) for bonds A & B Annual coupon rate (annual frequency) | 8% EAY | 9% Maturity (in years) Par 100100 (a) Current price (b) Macaulay duration (e) Modied duration (d) Convexity (e) Caleulate the actual price of the two bonds for a 100 basls point Inerease in interest rates (EAY) 0 Using duration, estimate the price of the bonds for a 100 basis polnt increase in interest rates (EAY) (g) Using duration & convexity, estimate the price of the bonds for a 100 basis point increase in interest rates (EAY) (h) Comment on the accuracy of your results in (f) and (g), and state why one approximation is closer to the actual price than the other

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts