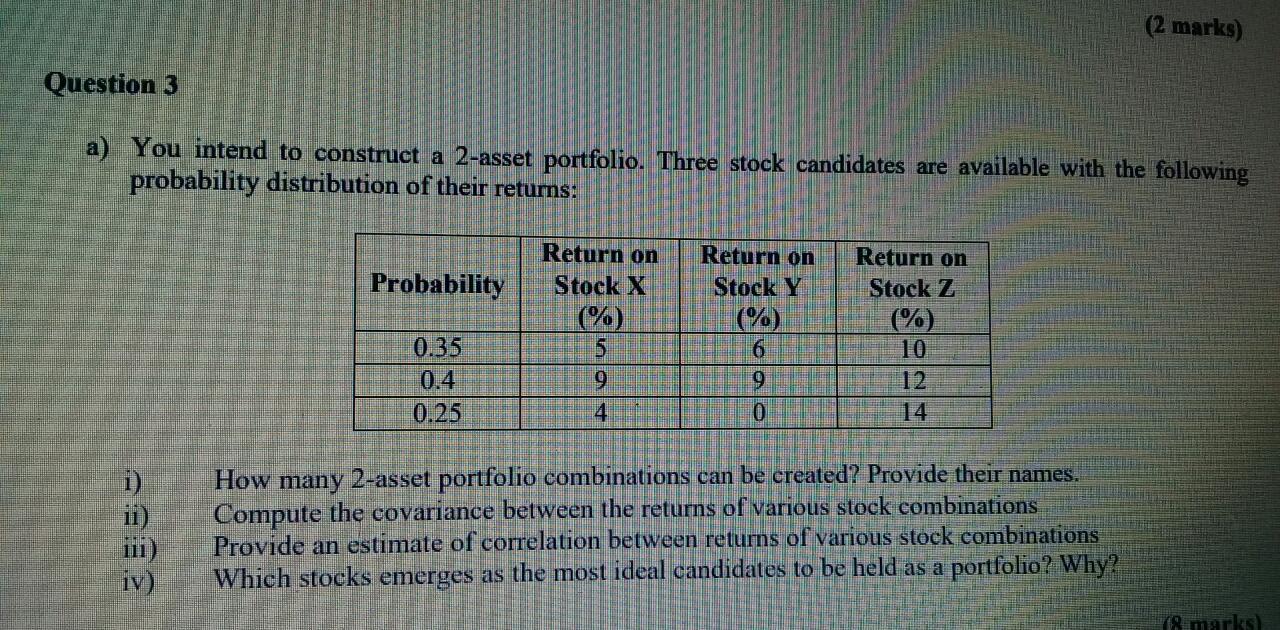

Question: (2 marks) Question 3 a) You intend to construct a 2-asset portfolio. Three stock candidates are available with the following probability distribution of their retums:

(2 marks) Question 3 a) You intend to construct a 2-asset portfolio. Three stock candidates are available with the following probability distribution of their retums: Probability Return on Stock X Return on Stock Y Probability Return on Stock Z (%) 10 12 14 6 0.35 0.4 0.25 5 9 4 0 i) ii) : How many 2-asset portfolio combinations can be created? Provide their names. Compute the covariance between the returns of various stock combinations Provide an estimate of correlation between retums of various stock combinations Which stocks emerges as the most ideal candidates to be held as a portfolio? Why? iv) (8 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock