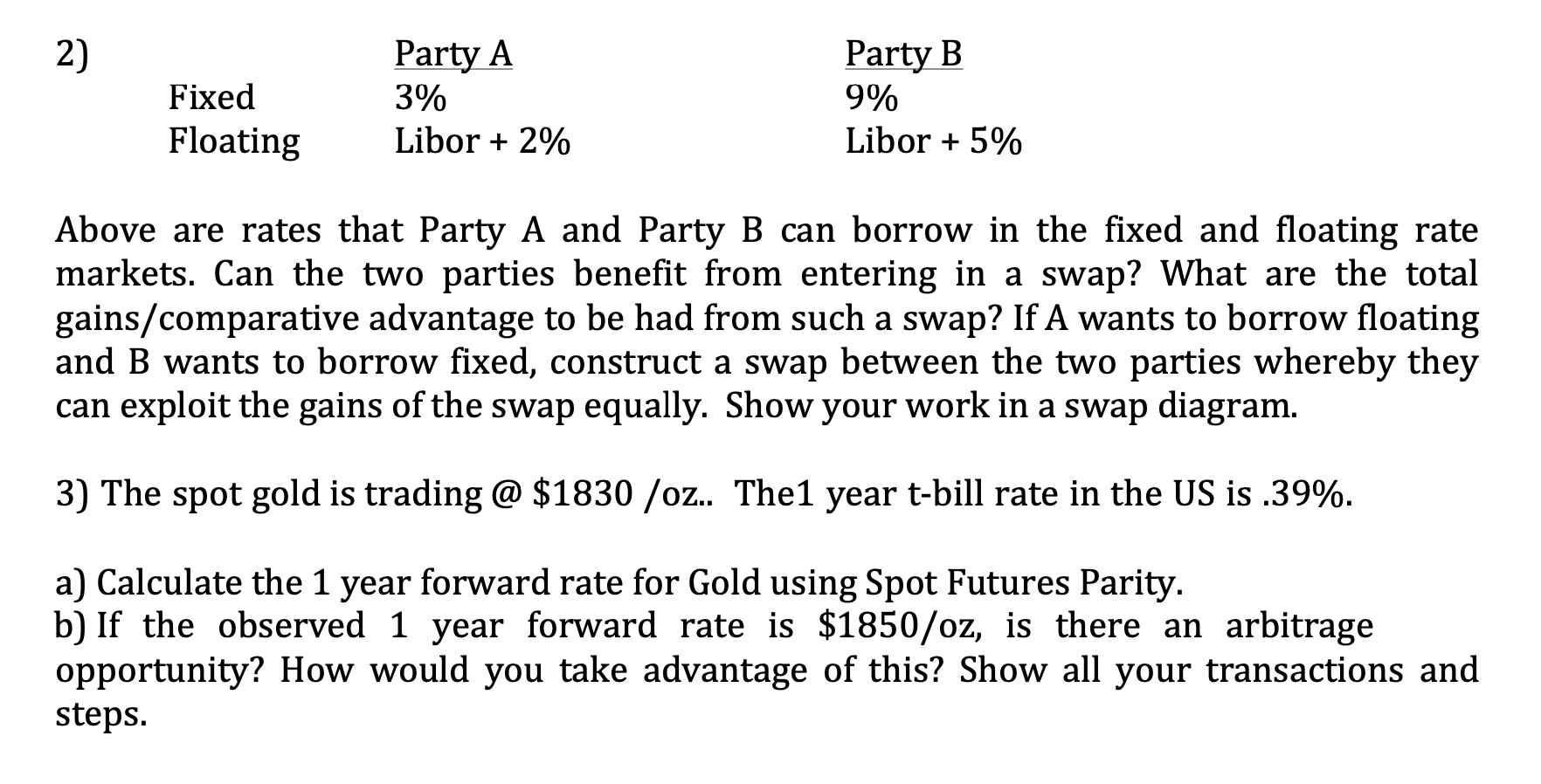

Question: 2) Party A Party B Fixed 3% 9% Floating Libor + 2% Libor + 5% Above are rates that Party A and Party B can

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts