Question: similar example Problem 8 (2 points): Both ABC and XYZ want to borrow $1,000,000 for 10 years. ABC wants to borrow at a floating interest

similar example

similar example

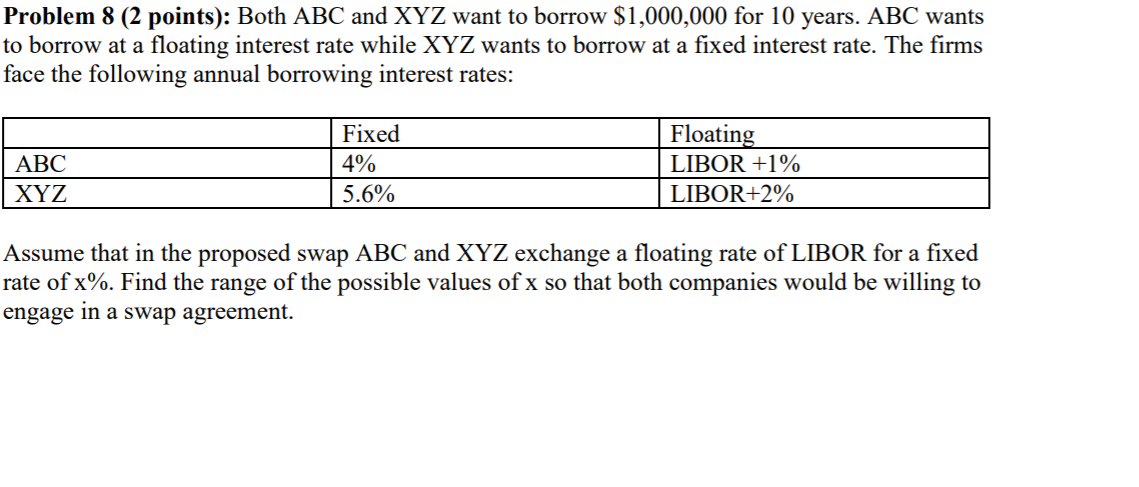

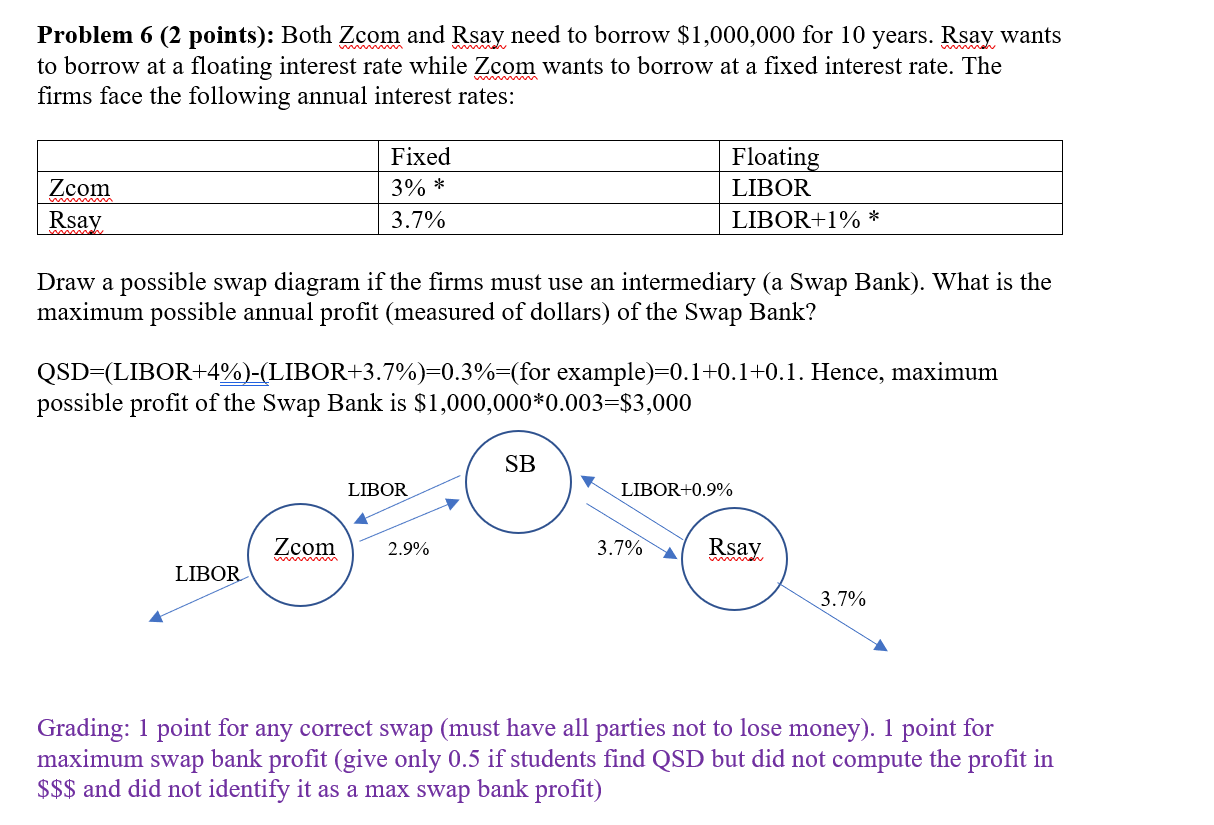

Problem 8 (2 points): Both ABC and XYZ want to borrow $1,000,000 for 10 years. ABC wants to borrow at a floating interest rate while XYZ wants to borrow at a fixed interest rate. The firms face the following annual borrowing interest rates: ABC XYZ Fixed 4% 5.6% Floating LIBOR +1% LIBOR+2% Assume that in the proposed swap ABC and XYZ exchange a floating rate of LIBOR for a fixed rate of x%. Find the range of the possible values of x so that both companies would be willing to engage in a swap agreement. Problem 6 (2 points): Both Zcom and Rsay need to borrow $1,000,000 for 10 years. Rsay wants to borrow at a floating interest rate while Zcom wants to borrow at a fixed interest rate. The firms face the following annual interest rates: Fixed 3%* Zcom Rsay Floating LIBOR LIBOR+1%* 3.7% Draw a possible swap diagram if the firms must use an intermediary (a Swap Bank). What is the maximum possible annual profit (measured of dollars) of the Swap Bank? QSD=(LIBOR+4%)-(LIBOR+3.7%)=0.3%=(for example)=0.1+0.1+0.1. Hence, maximum possible profit of the Swap Bank is $1,000,000*0.003=$3,000 SB LIBOR LIBOR+0.9% Zcom 2.9% 3.7% Rsay LIBOR 3.7% Grading: 1 point for any correct swap (must have all parties not to lose money). 1 point for maximum swap bank profit (give only 0.5 if students find QSD but did not compute the profit in $$$ and did not identify it as a max swap bank profit)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts