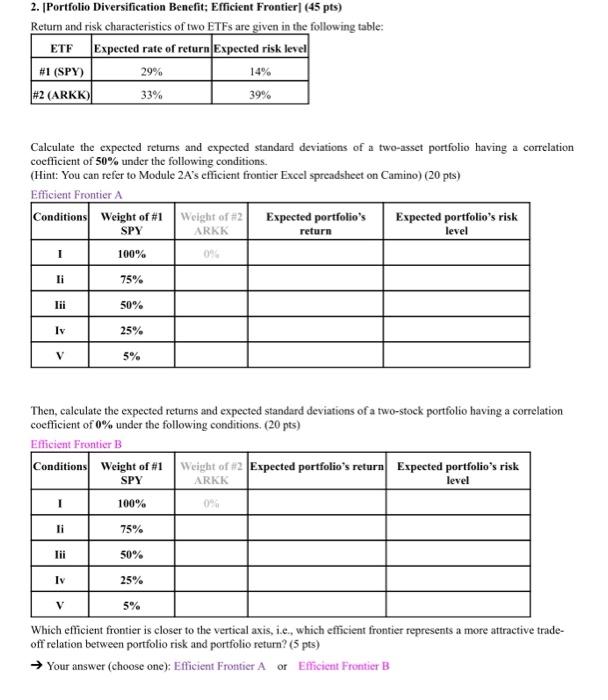

Question: 2. [Portfolio Diversification Benefit; Efficient Frontier (45 pts) Return and risk characteristics of two ETFs are given in the following table: ETE Expected rate of

2. [Portfolio Diversification Benefit; Efficient Frontier (45 pts) Return and risk characteristics of two ETFs are given in the following table: ETE Expected rate of return Expected risk level #1 (SPY) 29% 14% #2 (ARKK) 33% 39% Calculate the expected retums and expected standard deviations of a two-asset portfolio having a correlation coefficient of 50% under the following conditions (Hint: You can refer to Module 2A's efficient frontier Excel spreadsheet on Camino) (20 pts) Efficient Frontier A Conditions Weight of #1 Weight of #2 Expected portfolio's Expected portfolio's risk ARKK SPY return 100% 09 li 75% 50% 25% V 5% Then, calculate the expected returns and expected standard deviations of a two-stock portfolio having a correlation coefficient of 0% under the following conditions. (20 pts) Efficient Frontier B Conditions Weight of #1 Weight of #2 Expected portfolio's return Expected portfolio's risk SPY ARKK level 1 100% 0 75% lii 50% Iv 25% V 5% Which efficient frontier is closer to the vertical axis, i.e., which efficient frontier represents a more attractive trade- off relation between portfolio risk and portfolio return? (5 pts) Your answer (choose one): Efficient Frontier A or Efficient Frontier B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts