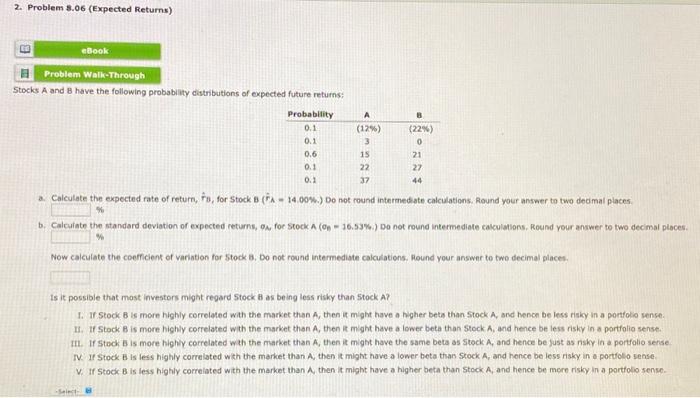

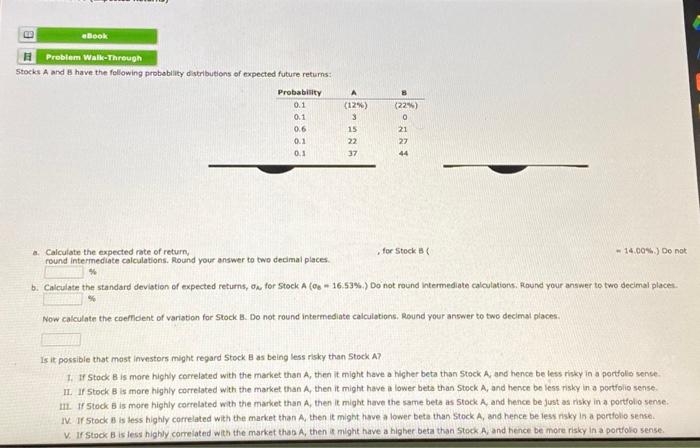

Question: 2. Problem 5.06 (Expected Returns) Stocks A and B have the following probability distributions of expected future returns: a. Calculate the expected rate of return,

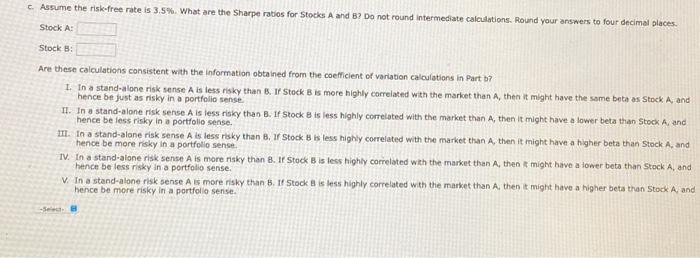

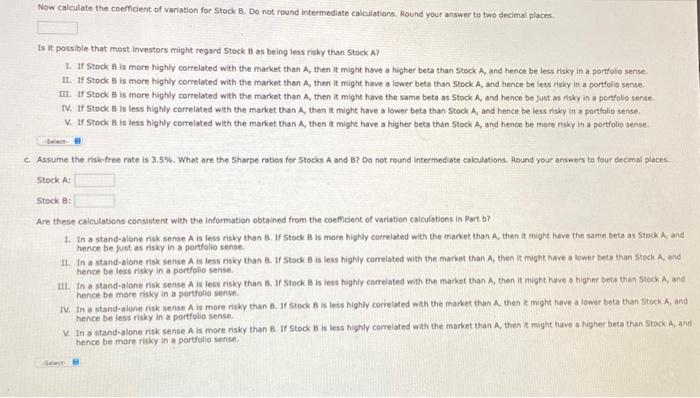

2. Problem 5.06 (Expected Returns) Stocks A and B have the following probability distributions of expected future returns: a. Calculate the expected rate of return, F^B, for S tock B(FA=14.00%.) Do not round intermed ate calculations. Round your answer to two dedmal places. \% b. Calcuiate the standard deviation of expected retums, for stock A(n=16.53%.) Do not round intermediate cakculations, Round vour answer to two decimal places. \% Now calculate the coefficient of variation for 5tock 8. Do not round intermediate calculations. Hound your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than 5 tock A? 1. If Stock B is more highly correloted wath the market than A, then it might have a higher beta than Stock A, and henon be less risky in a portfolio sense. 13. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio senst. II. If stock B is more highy correlated wat the market than A, then it might have the same beta as stock A, and hence be just as nsky in a portfolio sense N. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolo sense. V. If Stock B is less highly correlated with the market than A, then it might have a higher beta than stock A, and hence be mere risky in a portfolio sense. C. Assume the risk-free rate is 3,5%. What are the Sharpe ratios for 5 tocks A and B ? Do not round intermediate calculations. Round your answers to four decimal places: Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? I. In a stand-alone risk sense A is less risky than B, If Stock B is more highly carrelated with the market than A, then it might have the same beta os Stock A, and hence be fust as nisky in a portfolio sense. II. In a stand-alone risk sense A is less risky than B. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, ane hence be less risky in a portfolio sense. III. In a stand-alone risk sense A is less risky than B, If Stock B is less highy correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense IV. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market then A, then is might have a ioner beta than Stock A, and hence be less risky in a portfollo sense. V. In a stand-alone risk sense A ss more risky than B. If Stock B is less highly correlated with the market than A, then is might have a higher beta than Stock A, and hence be more risky in a portiolia sense. Stocks A and 8 have the fellowing probeblity distributions of expected future returns: a. Calculate the expected rate of return, , for 5 tock B ( =14.00%.) De nok round intermediate calculations. Round your answer to two dedmal places. \% b. Calculate the standard devistion of expected returns, for Stock A(b=16.53%. Do not round intermediate calculations: Flound your answer to two decimal place:. Now calculate the coeffident of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimsl places. Is if possible that mest investors might regard 5 tock B as being less risky than S tock A ? 1. If Stack B is mare highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfole senee. II. If 5 tock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as nsky in a portfolo sense. IV. If Stook 8 is less highly correlated with the market than A, then it might have a lower beta than stock A, and hence be less risky in a portiolo sente. V. If Stock B is less highly correlated with the market thas A, then is might have a higher beta than Stock A, and hence be more risky in a portfolio sense. Now calculate the coefficient of vartation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places Is it possble that most investors might regard Stock 8 as being less risky than 5 tock A ? 1. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolo sense. II. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be lest risicy in a portfol io sense. III. If Stock B is more highly correlated with the market than A, then it might have the same beto as 5 tock A, and hence be just as risk in a pertfolio sense: IV. If Stock B is less highly correlated with the market than A, then it might have a lower beto than stock A, and hence be less risky in a portlolio sense. V. If Stock B is less highly correlated with the market than A, then it might have a higher beta than 5 tock A, snd hence be more risky in a portiolio sense. C. Assume the risikfree rate is 3.5%. What are the Sharpe rotios for Stocks A and B? Do not round intermed ate calculations. Hound your answers to four decmal places. Stock A: Stock B : Are these calculations consistent with the information obtained from the coefledent of variation caiculations in Part b? 1. In a stand-alone risk sense A is less nisky than B. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as nisiy in a portelio sense. 11. In a stand-aione risk sende A is less nisky than a. if Stock B is less highly correlated with the market than A, then it might have a lower beta than Sreck A, and hence be less risky in a portfolio sense. II. In a standealone risk sense A is less nsky than B. If stock a is iess highly correiated with the market than A, then it might kave a higher beta trian stock A, and hence be mare risky in a portfolio sense. IV. In a stand-alone risk sense A is more riky than B. If stock A is less highly correlated with the market than A, then is might have a lower beta than 5tock A, and hence be less risky in a portfollo sense. V. In a stand-alone risk sense A is more risky than B. If Stock B is Hess highly correlated wat the market than A, then it might have a higher beta than stock A, an In a stand-abne rik sense Atsmore be more risky in a portfolio sense

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts