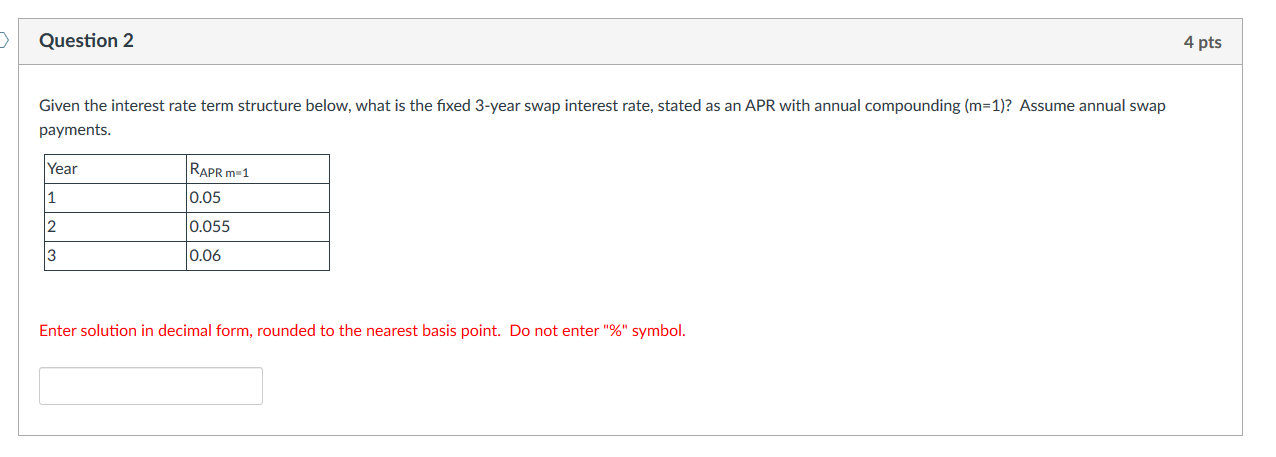

Question: 2 Question 2 4 pts Given the interest rate term structure below, what is the fixed 3-year swap interest rate, stated as an APR with

2 Question 2 4 pts Given the interest rate term structure below, what is the fixed 3-year swap interest rate, stated as an APR with annual compounding (m=1)? Assume annual swap payments. Year RAPR m-1 1 0.05 2 0.055 3 0.06 Enter solution in decimal form, rounded to the nearest basis point. Do not enter "%" symbol

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock