Question: (2) Question 3. Zero Lower Bound. In this question, we are interested in zero-coupon bond prices for nominal bonds. Under the expectations hypothesis, yt. 2(y

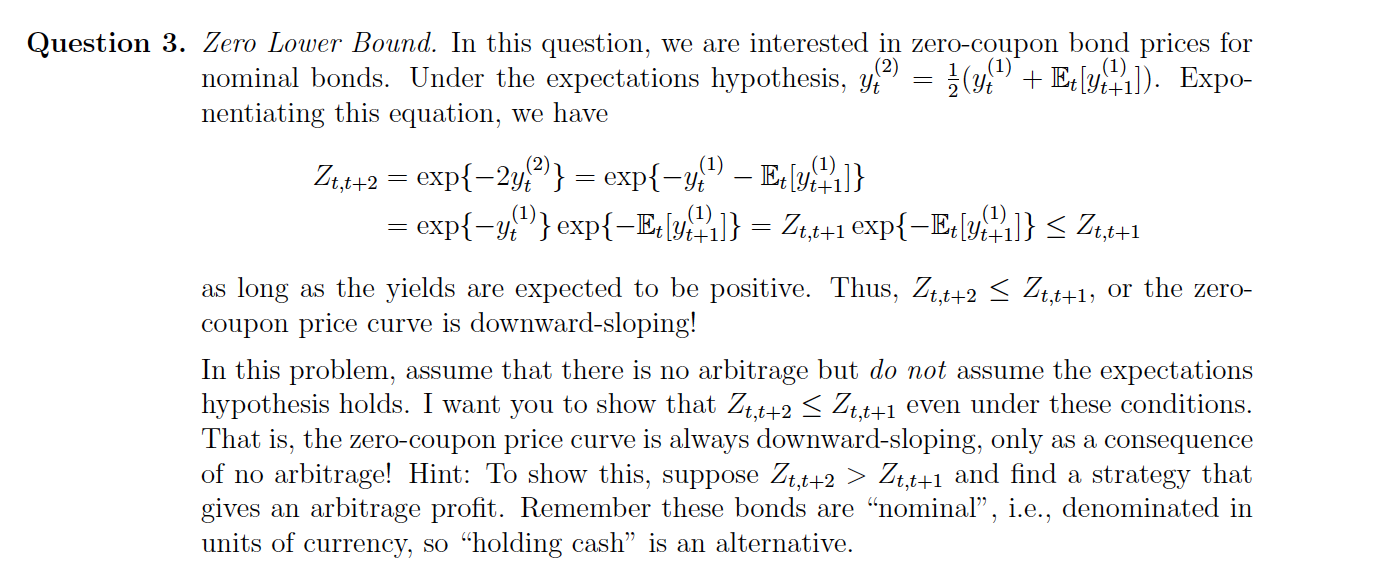

(2) Question 3. Zero Lower Bound. In this question, we are interested in zero-coupon bond prices for nominal bonds. Under the expectations hypothesis, yt. 2(y" + Et[y+1]). Expo- nentiating this equation, we have Z4,4+2 = exp{-24()} = exp{-y{") Ep[y{}}]} = exp{-4}}} exp{-Et[y{1}]} = Zt,x+1 exp{-Ex[y{1}]} Zt,t+1 and find a strategy that gives an arbitrage profit. Remember these bonds are nominal, i.e., denominated in units of currency, so "holding cash is an alternative. (2) Question 3. Zero Lower Bound. In this question, we are interested in zero-coupon bond prices for nominal bonds. Under the expectations hypothesis, yt. 2(y" + Et[y+1]). Expo- nentiating this equation, we have Z4,4+2 = exp{-24()} = exp{-y{") Ep[y{}}]} = exp{-4}}} exp{-Et[y{1}]} = Zt,x+1 exp{-Ex[y{1}]} Zt,t+1 and find a strategy that gives an arbitrage profit. Remember these bonds are nominal, i.e., denominated in units of currency, so "holding cash is an alternative

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts