Question: 2. Statistical measures of stand-alone risk Remember, the expected value of a probability distribution is a statistical measure of the average (mean) value expected to

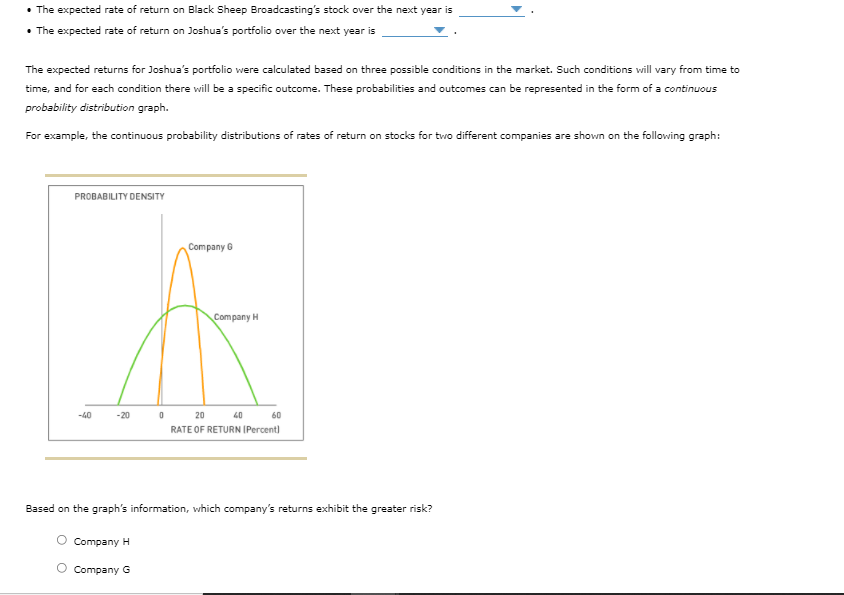

2. Statistical measures of stand-alone risk Remember, the expected value of a probability distribution is a statistical measure of the average (mean) value expected to occur during all possible circumstances. To compute an asset's expected return under a range of possible circumstances (or states of nature), multiply the anticipated return expected to result during each state of nature by its probability of occurrence. Consider the following case: Joshua owns a two-stock portfolio that invests in Happy Dog Soap Company (HDS) and Black Sheep Broadcasting (BSB). Three-quarters of Joshua's portfolio value consists of HDS's shares, and the balance consists of BSe's shares. Each stock's expected return for the next year will depend on forecasted market conditions. The expected returns from the stocks in different market conditions are detailed in the following table: Black Sheep Broadcasting Happy Dog Soap 32.5% 45.5% Market Condition Probability of Occurrence Strong 0.50 Normal 0.25 Weak 0.25 19.5% 26% -26% -32.5% Calculate expected returns for the individual stocks in Joshua's portfolio as well as the expected rate of return of the entire portfolio over the three possible market conditions next year. The expected rate of return on Happy Dog Soap's stock over the next year is The expected rate of return on Black Sheep Broadcasting's stock over the next year is The expected rate of return on Joshua's portfolio over the next year is The expected returns for Joshua's portfolio were calculated based on three possible conditions in the market. Such conditions will vary from time to time, and for each condition there will be a specific outcome. These probabilities and outcomes can be represented in the form of a continuous ncobability distribution aranh . The expected rate of return on Black Sheep Broadcasting's stock over the next year is The expected rate of return on Joshua's portfolio over the next year is The expected returns for Joshua's portfolio were calculated based on three possible conditions in the market. Such conditions will vary from time to time, and for each condition there will be a specific outcome. These probabilities and outcomes can be represented in the form of a continuous probability distribution graph. For example, the continuous probability distributions of rates of return on stocks for two different companies are shown on the following graph: PROBABILITY DENSITY Company G Company H -40 -20 0 20 40 60 RATE OF RETURN I Percent) Based on the graph's information, which company's returns exhibit the greater risk? Company H Company G

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts