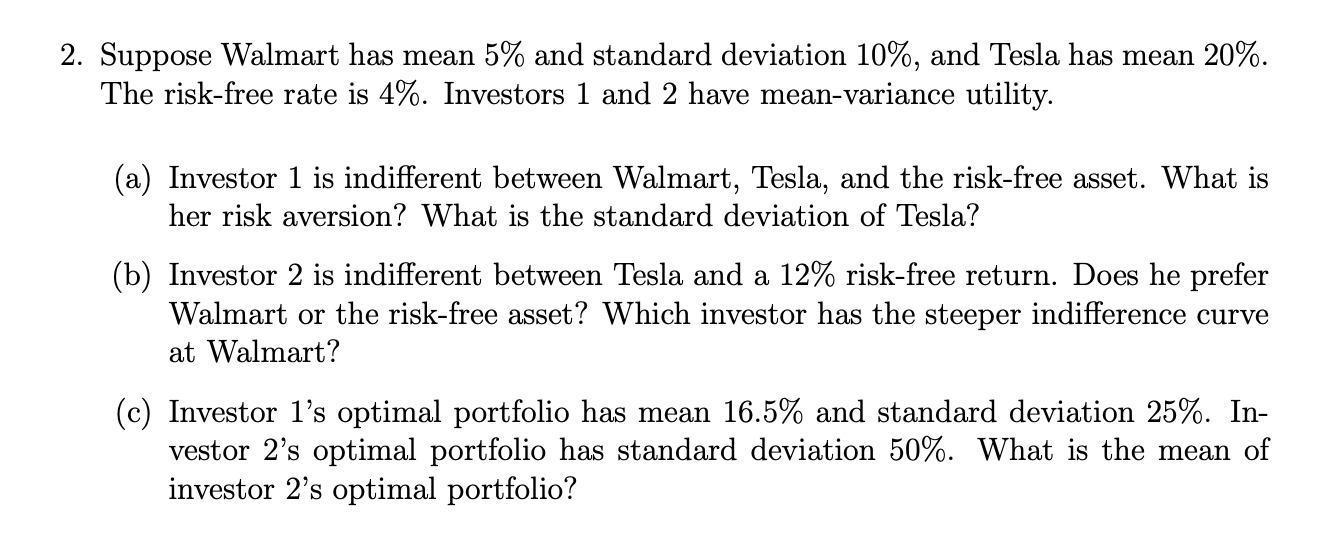

Question: 2. Suppose Walmart has mean 5% and standard deviation 10%, and Tesla has mean 20%. The risk-free rate is 4%. Investors 1 and 2 have

2. Suppose Walmart has mean 5% and standard deviation 10%, and Tesla has mean 20%. The risk-free rate is 4%. Investors 1 and 2 have mean-variance utility. (a) Investor 1 is indifferent between Walmart, Tesla, and the risk-free asset. What is her risk aversion? What is the standard deviation of Tesla? (b) Investor 2 is indifferent between Tesla and a 12% risk-free return. Does he prefer Walmart or the risk-free asset? Which investor has the steeper indifference curve at Walmart? (c) Investor 1's optimal portfolio has mean 16.5% and standard deviation 25%. In- vestor 2's optimal portfolio has standard deviation 50%. What is the mean of investor 2's optimal portfolio? 2. Suppose Walmart has mean 5% and standard deviation 10%, and Tesla has mean 20%. The risk-free rate is 4%. Investors 1 and 2 have mean-variance utility. (a) Investor 1 is indifferent between Walmart, Tesla, and the risk-free asset. What is her risk aversion? What is the standard deviation of Tesla? (b) Investor 2 is indifferent between Tesla and a 12% risk-free return. Does he prefer Walmart or the risk-free asset? Which investor has the steeper indifference curve at Walmart? (c) Investor 1's optimal portfolio has mean 16.5% and standard deviation 25%. In- vestor 2's optimal portfolio has standard deviation 50%. What is the mean of investor 2's optimal portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts