Question: 2. The table below gives the historical return data for Amazon and Exxon-Mobile from the past year. Each indicated return rate is end-of-month to end-of-month

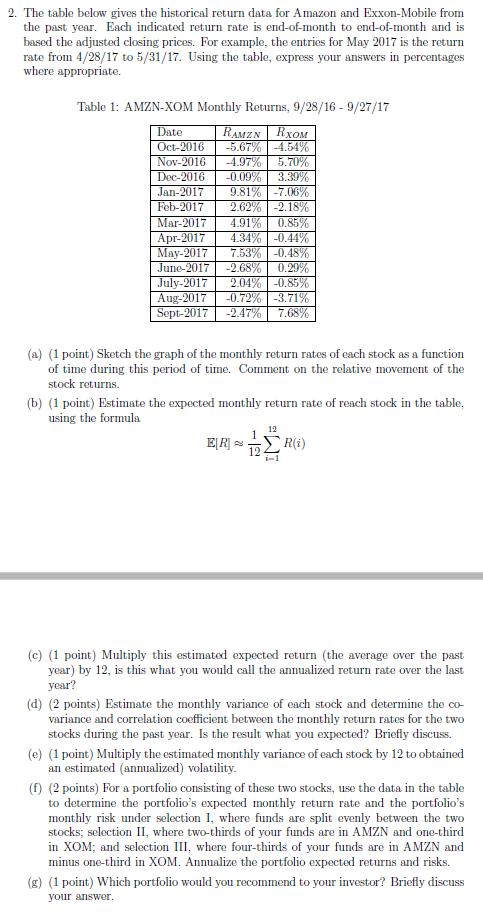

2. The table below gives the historical return data for Amazon and Exxon-Mobile from the past year. Each indicated return rate is end-of-month to end-of-month and is based the adjusted closing prices. For example, the entries for May 2017 is the return rate from 4/28/17 to 5/31/17. Using the table, express your answers in percentages where appropriate. Table 1: AMZN-XOM Monthly Returns, 9/28/16 - 9/27/17 te MZN OM Oct-2016 5.67% 4.54% ov-2016 81 62 an-2017 18 ar-2017 pr-201 ay-2017 une-2017 ily-2017| 2.04%|-0.85% 53% | -0.48% 2.68%| 0 7.68 (a) 1 point) Sketch the graph of the monthly return rates of each stock as a function of time during this period of time. Comment on the relative movement of the stock returns. (b) (1 point) Estimate the expected monthly return rate of reach stock in the table, using the formula 12 12 (c) (1 point) Multiply this estimated expected return (the average over the past year) by 12, is this what you would call the annualized return rate over the last year? (d) (2 points) Estimate the monthly variance of each stock and determine the co- variance and correlation coefficient between the monthly return rates for the two stocks during the past year. Is the result what you expected? riefly discuss. (e) (1 point) Multiply the estimated monthly variance of each stock by 12 to obtained an estimated (annualized) volatility. (f) (2 points) For a portfolio consisting of these two stocks, use the data in the table to determine the portfolio's expected monthly return rate and the portfolio's monthly risk under selection I, where funds are split evenly between the two stocks; selection I, where two-thirds of your funds are in AMZN and one-third in XOM; and selectionII, where four-thirds of your funds are in AMZN and minus one-third in XOM. Annualize the portfolio expected returns and risks. (g) (1 point) Which portfolio would you recommend to your investor? Briefly discuss your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts