Question: 2. (Two securities) Consider a portfolio with two securities having returns Mi and M2, risks 01 and 02, and a correlation coefficient p that vanishes.

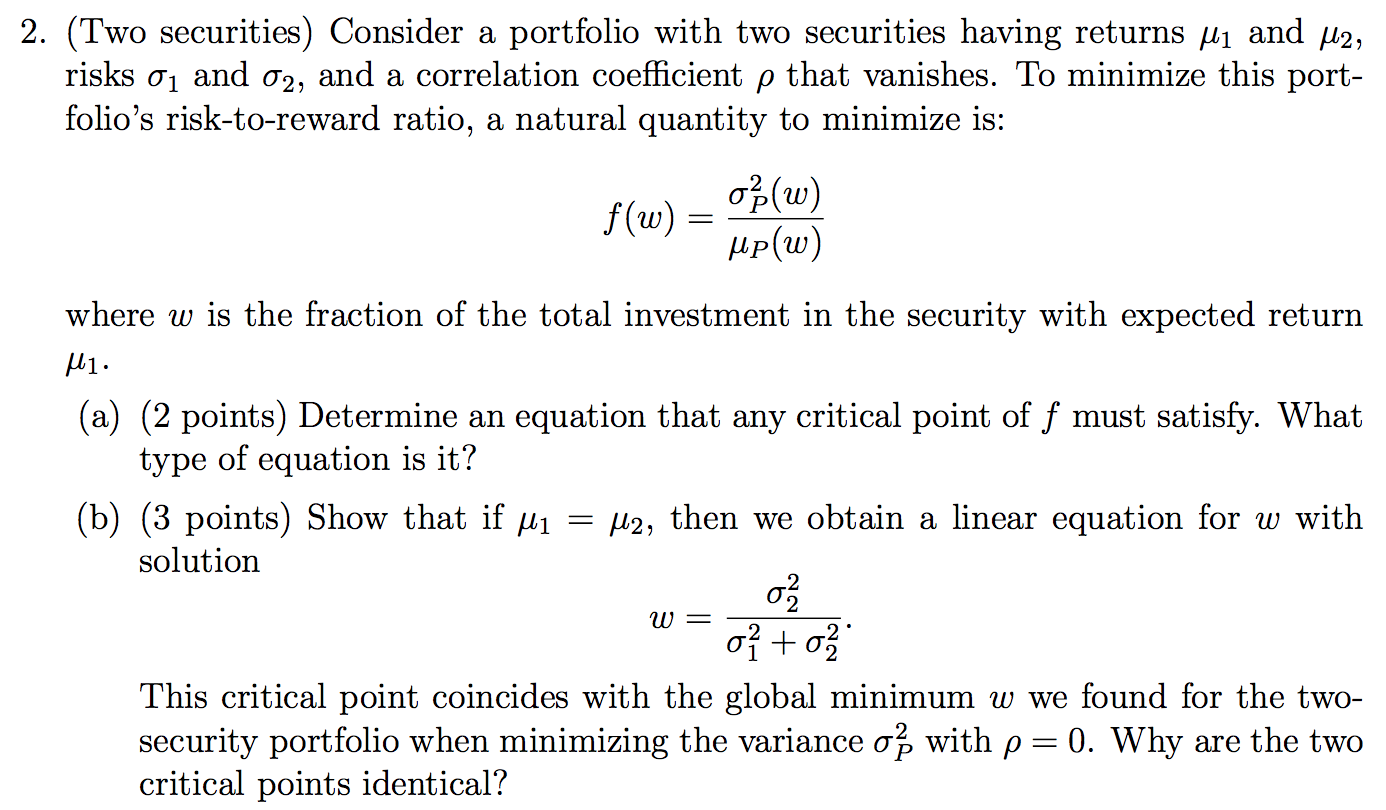

2. (Two securities) Consider a portfolio with two securities having returns Mi and M2, risks 01 and 02, and a correlation coefficient p that vanishes. To minimize this port- folio's risk-to-reward ratio, a natural quantity to minimize is: f(w) 0(W) Mp(w) where w is the fraction of the total investment in the security with expected return M1. (a) (2 points) Determine an equation that any critical point of f must satisfy. What type of equation is it? (b) (3 points) Show that if M1 = M2, then we obtain a linear equation for w with solution W o +o This critical point coincides with the global minimum w we found for the two- security portfolio when minimizing the variance o with p=0. Why are the two critical points identical? 2. (Two securities) Consider a portfolio with two securities having returns Mi and M2, risks 01 and 02, and a correlation coefficient p that vanishes. To minimize this port- folio's risk-to-reward ratio, a natural quantity to minimize is: f(w) 0(W) Mp(w) where w is the fraction of the total investment in the security with expected return M1. (a) (2 points) Determine an equation that any critical point of f must satisfy. What type of equation is it? (b) (3 points) Show that if M1 = M2, then we obtain a linear equation for w with solution W o +o This critical point coincides with the global minimum w we found for the two- security portfolio when minimizing the variance o with p=0. Why are the two critical points identical

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts