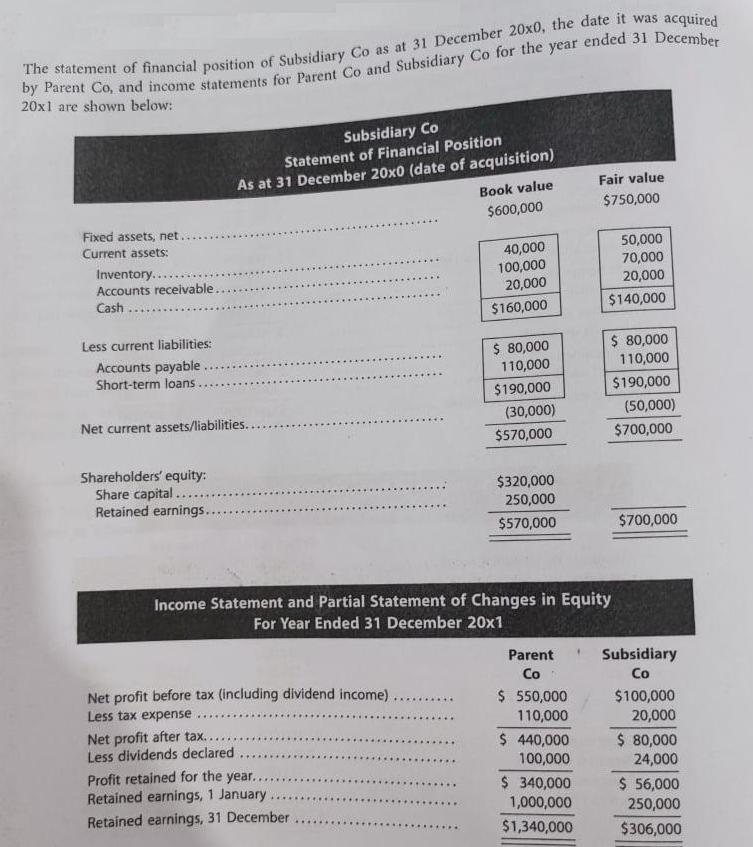

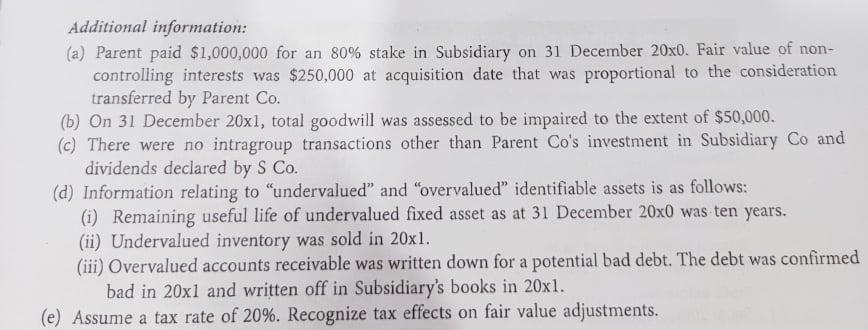

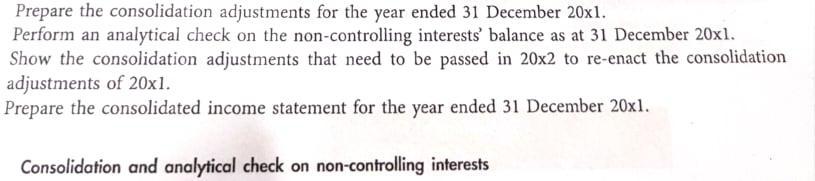

The statement of financial position of Subsidiary Co as at 31 December 20x0, the date it...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Accounting Business Reporting for Decision Making

ISBN: 9780730302414

4th edition

Authors: Jacqueline Birt, Keryn Chalmers, Albie Brooks, Suzanne Byrne, Judy Oliver

Posted Date: