Question: 2-1. There are three assets with mean vector, and variance- covariance matrix. | have $10,000 and the investment proportion for asset 1 is 20%, for

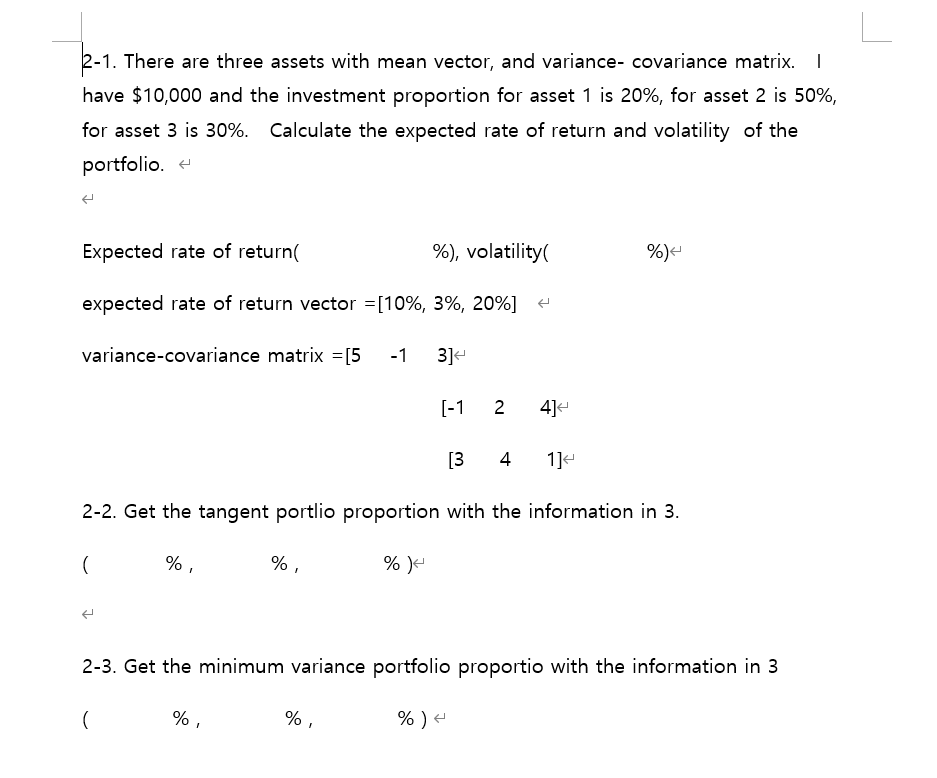

2-1. There are three assets with mean vector, and variance- covariance matrix. | have $10,000 and the investment proportion for asset 1 is 20%, for asset 2 is 50%, for asset 3 is 30%. Calculate the expected rate of return and volatility of the portfolio. + Expected rate of return %), volatility %) expected rate of return vector = [10%, 3%, 20%] H variance-covariance matrix = [5 -1 3] [-1 2 4] [3 4 1] 2-2. Get the tangent portlio proportion with the information in 3. ( % % % 1 2-3. Get the minimum variance portfolio proportio with the information in 3 ( % %, % )

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock