2-year SOFR/Tsy spread update 1. Calculate the net profit or loss on the 2-year SOFR/Tsy spread trade

Question:

2-year SOFR/Tsy spread update

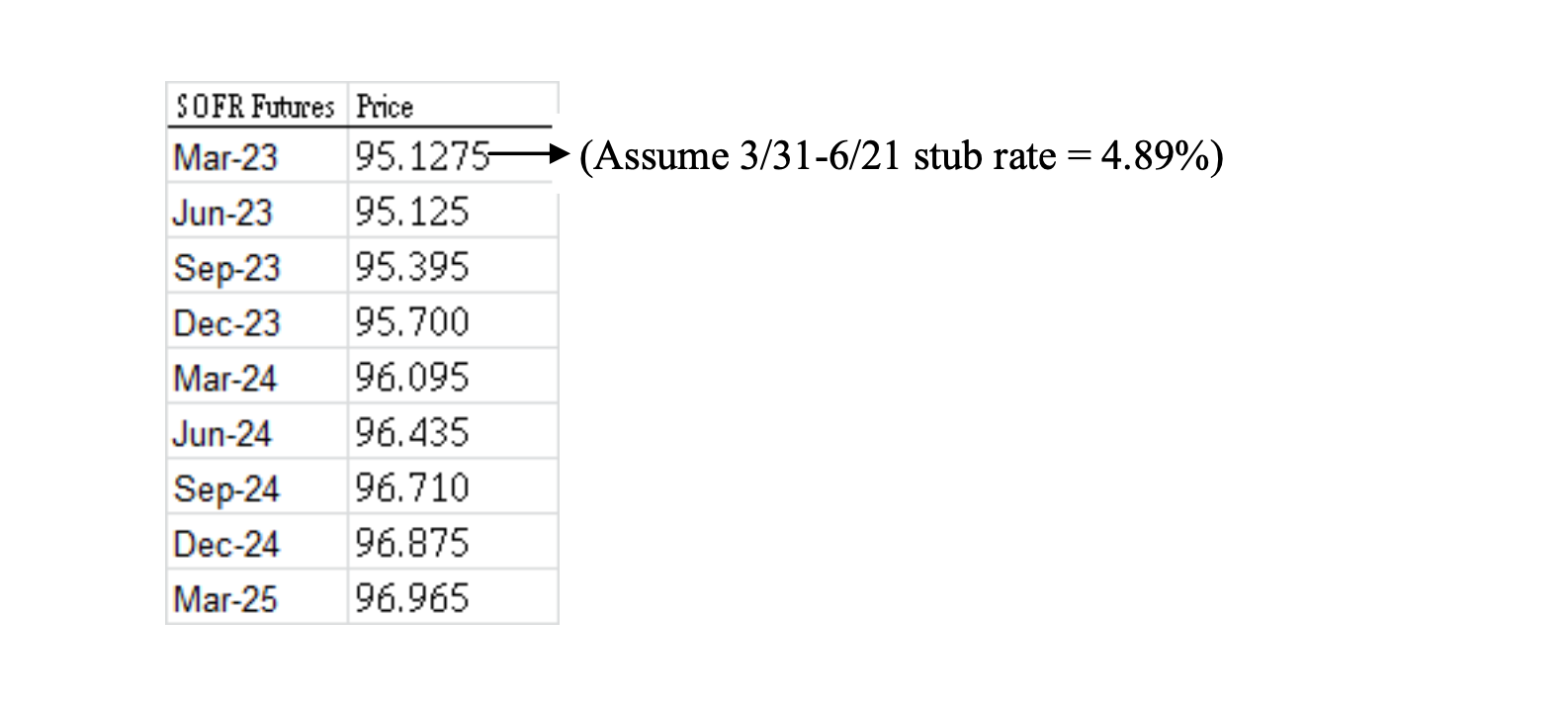

1. Calculate the net profit or loss on the 2-year SOFR/Tsy spread trade over the past week, using prices as of Friday, March 31. Include in your profit calculation the coupon income earned on the 2-year Treasury net of the cost of financing the position over a one week (7 day) period. SOFR futures prices as of March 31 are as follows:

4-5/8% of 2/25: Full price: 101.35504

1-week repo (7 days): 4.9% (you can use this to calculate financing cost on the Treasury)

2. Recalculate your SOFR futures hedge as of March 31 and update the SOFR/Tsy Futures spread table distributed last week.

Expert Answer:

Anwers To calculate the net profit or loss on the 2year SOFRTsy spread trade over the past week we need to consider the following 1 The cost of financing the position This can be calculated by multipl... View the full answer

Fundamental Accounting

ISBN: 9781485112112

7th Edition

Authors: David Flynn, Carolina Koornhof, Ronald Arendse, Anna C. E. Coetzee, Edwardo Muriro, Louise Christel Posthumus, Louise Mancy Smit