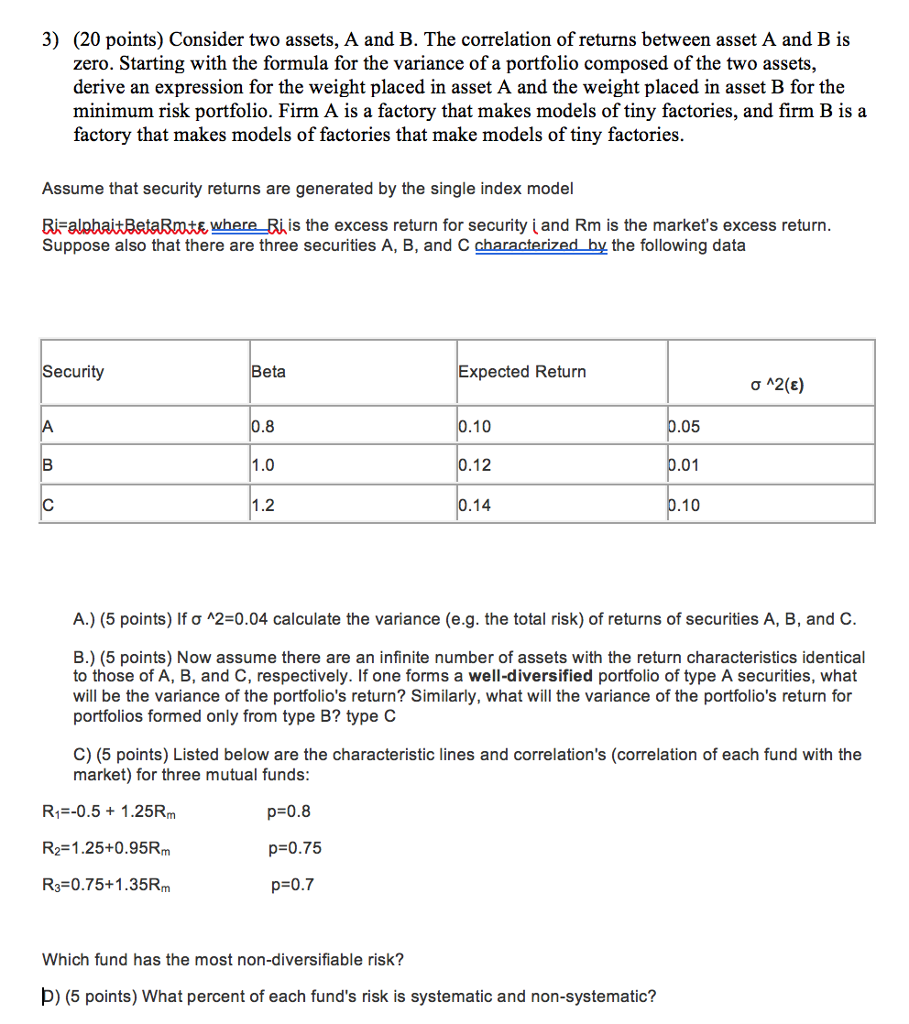

Question: 3) (20 points) Consider two assets, A and B. The correlation of returns between asset A and B is zero. Starting with the formula for

3) (20 points) Consider two assets, A and B. The correlation of returns between asset A and B is zero. Starting with the formula for the variance of a portfolio composed of the two assets, derive an expression for the weight placed in asset A and the weight placed in asset B for the minimum risk portfolio. Firm A is a factory that makes models of tiny factories, and firm B is a factory that makes models of factories that make models of tiny factories. Assume that security returns are generated by the single index model R,-alpha?As taR00??where Ris the excess return for security i and Rm is the market's excess return Suppose also that there are three securities A, B, and C characterized by the following data ecurity Beta Expected Return 05 01 10 10 12 1.2 A.) (5 points) If ? ^2-0.04 calculate the variance (eg. the total risk) of returns of securities A, B, and C B.) (5 points) Now assume there are an infinite number of assets with the return characteristics identical to those of A, B, and C, respectively. If one forms a well-diversified portfolio of type A securities, what will be the variance of the portfolio's return? Similarly, what will the variance of the portfolio's return for portfolios formed only from type B? type C C) (5 points) Listed below are the characteristic lines and correlation's (correlation of each fund with the market) for three mutual funds R1-0.5 1.25Rnm R2-1.25+0.95Rm R3-0.75+1.35Rm p=0.8 p 0.75 p 0.7 Which fund has the most non-diversifiable risk D) (5 points) What percent of each fund's risk is systematic and non-systematic? 3) (20 points) Consider two assets, A and B. The correlation of returns between asset A and B is zero. Starting with the formula for the variance of a portfolio composed of the two assets, derive an expression for the weight placed in asset A and the weight placed in asset B for the minimum risk portfolio. Firm A is a factory that makes models of tiny factories, and firm B is a factory that makes models of factories that make models of tiny factories. Assume that security returns are generated by the single index model R,-alpha?As taR00??where Ris the excess return for security i and Rm is the market's excess return Suppose also that there are three securities A, B, and C characterized by the following data ecurity Beta Expected Return 05 01 10 10 12 1.2 A.) (5 points) If ? ^2-0.04 calculate the variance (eg. the total risk) of returns of securities A, B, and C B.) (5 points) Now assume there are an infinite number of assets with the return characteristics identical to those of A, B, and C, respectively. If one forms a well-diversified portfolio of type A securities, what will be the variance of the portfolio's return? Similarly, what will the variance of the portfolio's return for portfolios formed only from type B? type C C) (5 points) Listed below are the characteristic lines and correlation's (correlation of each fund with the market) for three mutual funds R1-0.5 1.25Rnm R2-1.25+0.95Rm R3-0.75+1.35Rm p=0.8 p 0.75 p 0.7 Which fund has the most non-diversifiable risk D) (5 points) What percent of each fund's risk is systematic and non-systematic

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts