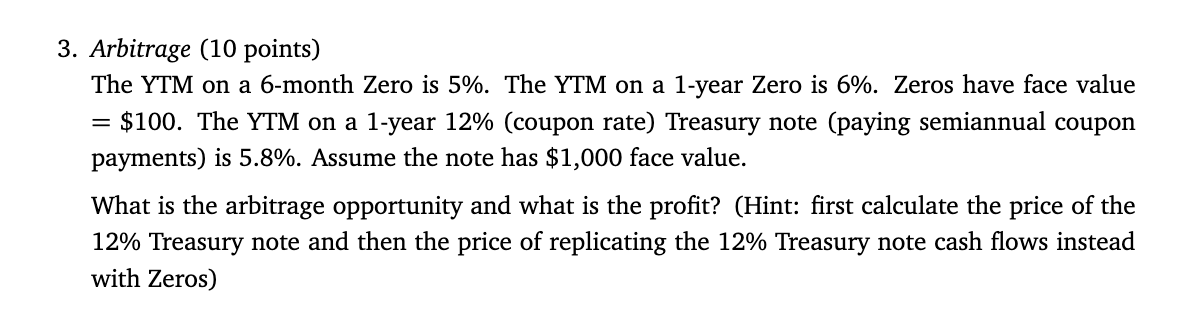

Question: 3 . Arbitrage ( 1 0 points ) The YTM on a 6 - month Zero is ( 5 % ) .

Arbitrage points The YTM on a month Zero is The YTM on a year Zero is Zeros have face value $ The YTM on a year coupon rate Treasury note paying semiannual coupon payments is Assume the note has $ face value. What is the arbitrage opportunity and what is the profit? Hint: first calculate the price of the Treasury note and then the price of replicating the Treasury note cash flows instead with Zeros

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock