Question: 3. Assume that the following one-factor model describes the expected return for portfolios: E(R) 0.10 +0.12p,1 Also assume that all investors agree on the

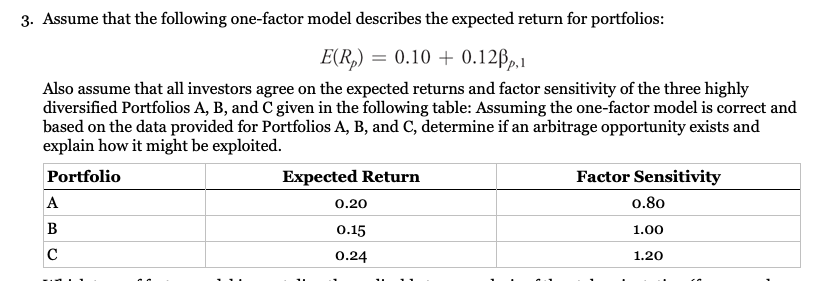

3. Assume that the following one-factor model describes the expected return for portfolios: E(R) 0.10 +0.12p,1 Also assume that all investors agree on the expected returns and factor sensitivity of the three highly diversified Portfolios A, B, and C given in the following table: Assuming the one-factor model is correct and based on the data provided for Portfolios A, B, and C, determine if an arbitrage opportunity exists and explain how it might be exploited. Portfolio A B C Expected Return 0.20 0.15 0.24 Factor Sensitivity 0.80 1.00 1.20

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock