Question: 3 | | | . AUT AFT Part 2 (Application) Suppose that you have to sell an asset (in pound unit) in 3 months from

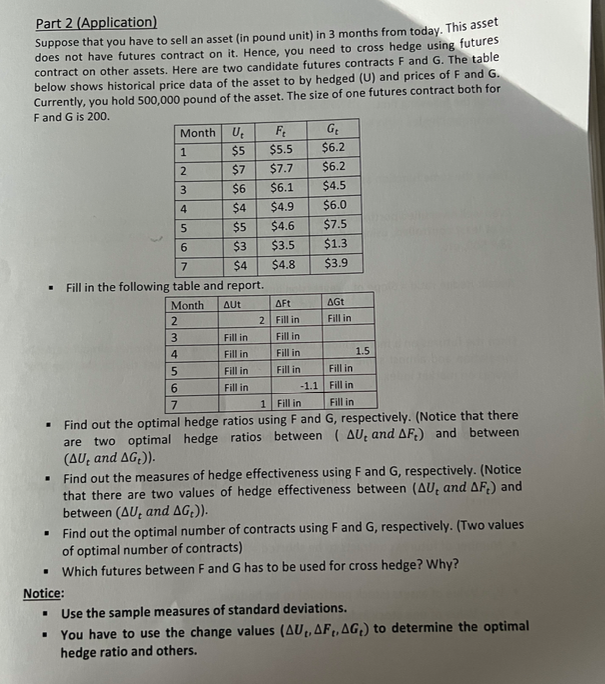

3 | | | . AUT AFT Part 2 (Application) Suppose that you have to sell an asset (in pound unit) in 3 months from today. This asset does not have futures contract on it. Hence, you need to cross hedge using futures contract on other assets. Here are two candidate futures contracts F and G. The table below shows historical price data of the asset to by hedged (U) and prices of F and G. Currently, you hold 500,000 pound of the asset. The size of one futures contract both for Fand G is 200. Month U F G 1 $5 $5.5 $6.2 2 $7 $7.7 $6.2 $6 $6.1 $4.5 4 $4 $4.9 $6.0 5 $5 $4.6 $7.5 6 $3 $3.5 $1.3 7 $4 $4.8 $3.9 Fill in the following table and report. Month AGE 2 2 Fill in Fill in 3 Fill in Fill in 4 Fill in Fill in 1.5 5 Fill in Fill in Fill in 6 Fill in -1.1 Fill in 7 1 Fill in Fill in Find out the optimal hedge ratios using F and G, respectively. (Notice that there are two optimal hedge ratios between ( AU, and AF) and between (AU, and AG.)). Find out the measures of hedge effectiveness using F and G, respectively. (Notice that there are two values of hedge effectiveness between (AU, and AF) and between (AU, and AG)). Find out the optimal number of contracts using Fand G, respectively. (Two values of optimal number of contracts) Which futures between F and G has to be used for cross hedge? Why? Notice: Use the sample measures of standard deviations. You have to use the change values (AU, AF, AG) to determine the optimal hedge ratio and others

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts