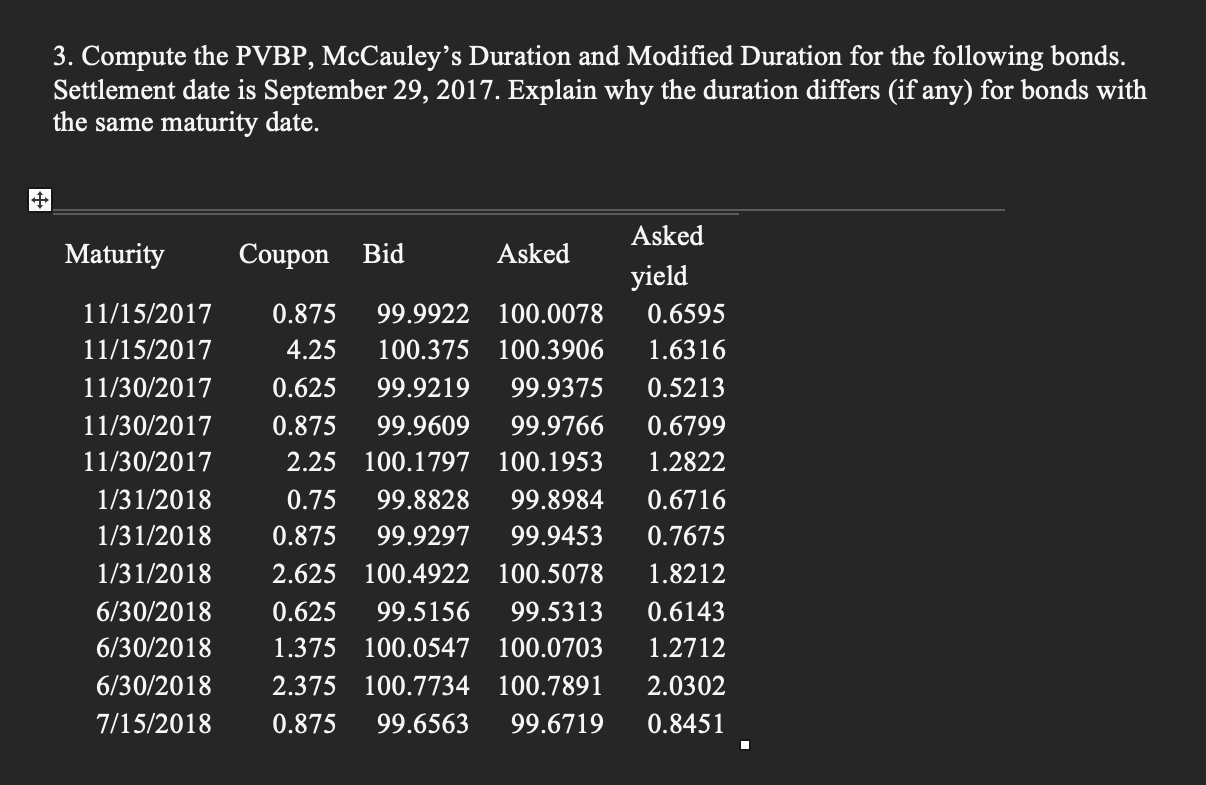

Question: + 3. Compute the PVBP, McCauley's Duration and Modified Duration for the following bonds. Settlement date is September 29, 2017. Explain why the duration

+ 3. Compute the PVBP, McCauley's Duration and Modified Duration for the following bonds. Settlement date is September 29, 2017. Explain why the duration differs (if any) for bonds with the same maturity date. Asked Maturity Coupon Bid Asked yield 11/15/2017 0.875 99.9922 100.0078 0.6595 11/15/2017 11/30/2017 4.25 100.375 100.3906 0.625 99.9219 99.9375 1.6316 0.5213 11/30/2017 0.875 99.9609 99.9766 0.6799 11/30/2017 2.25 100.1797 100.1953 1.2822 1/31/2018 0.75 99.8828 99.8984 0.6716 1/31/2018 1/31/2018 0.875 99.9297 2.625 100.4922 100.5078 99.9453 0.7675 1.8212 6/30/2018 0.625 99.5156 99.5313 0.6143 6/30/2018 1.375 100.0547 100.0703 1.2712 6/30/2018 2.375 100.7734 100.7891 2.0302 7/15/2018 0.875 99.6563 99.6719 0.8451

Step by Step Solution

There are 3 Steps involved in it

Answer To compute the PVBP Price Value of a Basis Point McCauleys Duration and Modified Duration for ... View full answer

Get step-by-step solutions from verified subject matter experts