Question: 3. Consider Mean-Variance analysis to construct the optimal portfolio. The relevant sample statistics are summarized in the table below and an investor i's utility function

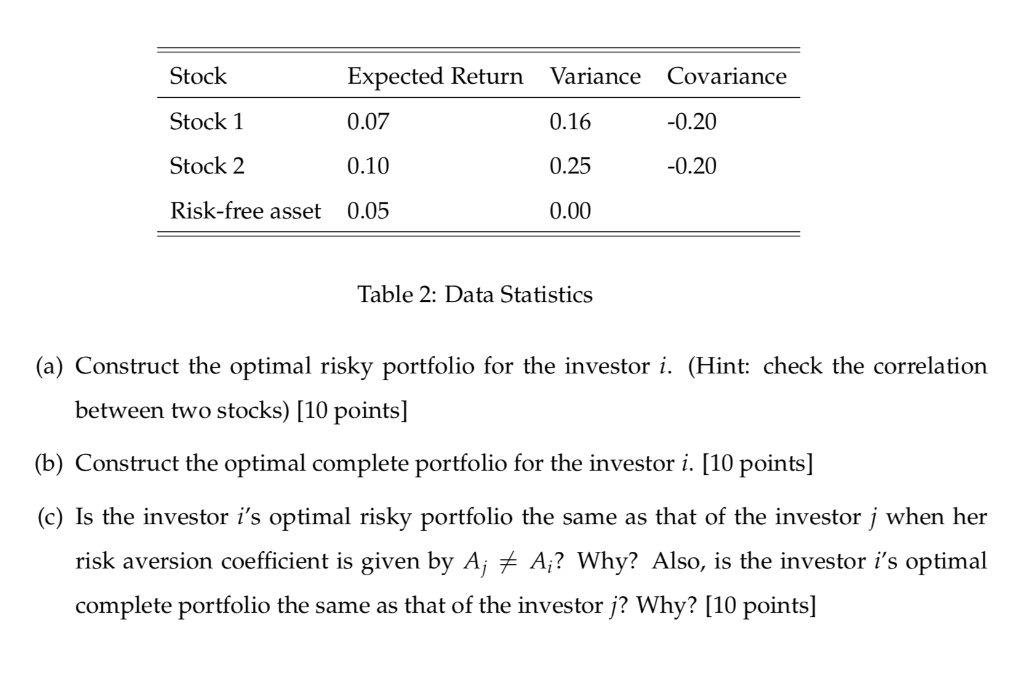

3. Consider Mean-Variance analysis to construct the optimal portfolio. The relevant sample statistics are summarized in the table below and an investor i's utility function is given by U; = 100E(rc) A;100-Var(rc). (2) Stock Variance Covariance Expected Return 0.07 Stock 1 0.16 -0.20 Stock 2 0.10 0.25 -0.20 Risk-free asset 0.05 0.00 Table 2: Data Statistics (a) Construct the optimal risky portfolio for the investor i. (Hint: check the correlation between two stocks) (10 points] (b) Construct the optimal complete portfolio for the i. [10 points) (c) Is the investor i's optimal risky portfolio the same as that of the investor j when her risk aversion coefficient is given by Aj + A? Why? Also, is the investor is optimal complete portfolio the same as that of the investor j? Why? [10 points] 3. Consider Mean-Variance analysis to construct the optimal portfolio. The relevant sample statistics are summarized in the table below and an investor i's utility function is given by U; = 100E(rc) A;100-Var(rc). (2) Stock Variance Covariance Expected Return 0.07 Stock 1 0.16 -0.20 Stock 2 0.10 0.25 -0.20 Risk-free asset 0.05 0.00 Table 2: Data Statistics (a) Construct the optimal risky portfolio for the investor i. (Hint: check the correlation between two stocks) (10 points] (b) Construct the optimal complete portfolio for the i. [10 points) (c) Is the investor i's optimal risky portfolio the same as that of the investor j when her risk aversion coefficient is given by Aj + A? Why? Also, is the investor is optimal complete portfolio the same as that of the investor j? Why? [10 points]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts