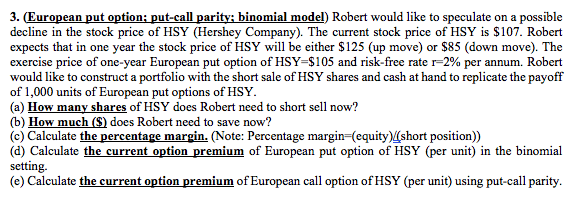

Question: 3. (European put option: put-call parity: binomial model) Robert would like to speculate on a possible decline in the stock price of HSY (Hershey Company).

3. (European put option: put-call parity: binomial model) Robert would like to speculate on a possible decline in the stock price of HSY (Hershey Company). The current stock price of HSY is $107. Robert expects that in one year the stock price of HSY will be either $125 (up move) or $85 (down move). The exercise price of one-year European put option of HSY-$105 and risk-free rate r=2% per annum. Robert would like to construct a portfolio with the short sale of HSY shares and cash at hand to replicate the payoff of 1,000 units of European put options of HSY. (a) How many shares of HSY does Robert need to short sell now? (b) How much (S) does Robert need to save now? (c) Calculate the percentage margin. (Note: Percentage margin (equity)short position) (d) Calculate the current option premium of European put option of HSY (per unit) in the binomial setting. (e) Calculate the current option premium of European call option of HSY (per unit) using put-call parity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts