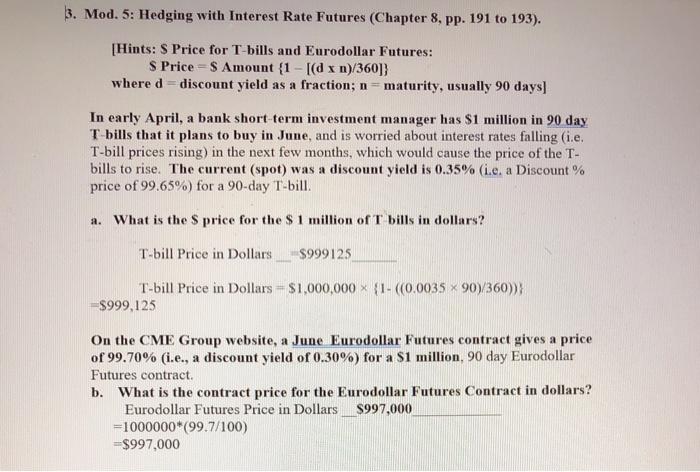

Question: 3. Mod. 5: Hedging with Interest Rate Futures (Chapter 8, pp. 191 to 193). [Hints: S Price for T-bills and Eurodollar Futures: S Price =

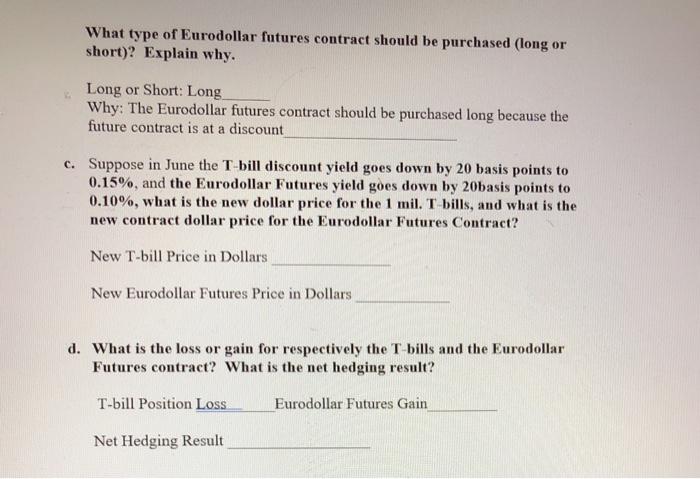

3. Mod. 5: Hedging with Interest Rate Futures (Chapter 8, pp. 191 to 193). [Hints: S Price for T-bills and Eurodollar Futures: S Price = $ Amount {1- (d xn)/360]} where d-discount yield as a fraction; n -- maturity, usually 90 days) In early April, a bank short-term investment manager has $1 million in 90 day T bills that it plans to buy in June, and is worried about interest rates falling (i.e. T-bill prices rising) in the next few months, which would cause the price of the T- bills to rise. The current (spot) was a discount yield is 0.35% (ie, a Discount % price of 99.65%) for a 90-day T-bill. a. What is the price for the $ 1 million of T bills in dollars? T-bill Price in Dollars $999125 T-bill Price in Dollars - $1,000,000 > {1- ((0.0035 x 90)/360))} =$999,125 On the CME Group website, a June Eurodollar Futures contract gives a price of 99.70% (i.e., a discount yield of 0.30%) for a $1 million, 90 day Eurodollar Futures contract b. What is the contract price for the Eurodollar Futures Contract in dollars? Eurodollar Futures Price in Dollars $997,000 =1000000*(99.7/100) =$997,000 What type of Eurodollar futures contract should be purchased (long or short)? Explain why. Long or Short: Long Why: The Eurodollar futures contract should be purchased long because the future contract is at a discount c. Suppose in June the T-bill discount yield goes down by 20 basis points to 0.15%, and the Eurodollar Futures yield goes down by 20basis points to 0.10%, what is the new dollar price for the 1 mil. T bills, and what is the new contract dollar price for the Eurodollar Futures Contract? New T-bill Price in Dollars New Eurodollar Futures Price in Dollars d. What is the loss or gain for respectively the T-bills and the Eurodollar Futures contract? What is the net hedging result? T-bill Position Loss Eurodollar Futures Gain Net Hedging Result

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts