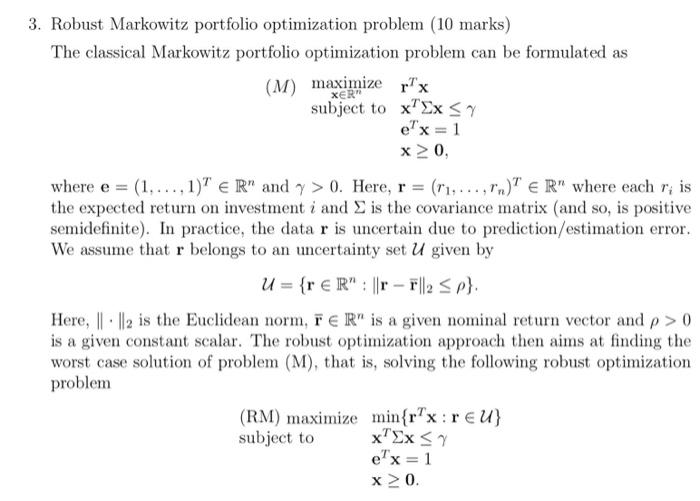

Question: 3. Robust Markowitz portfolio optimization problem (10 marks) The classical Markowitz portfolio optimization problem can be formulated as (M) maximizer subject to xEx 57 e'x

3. Robust Markowitz portfolio optimization problem (10 marks) The classical Markowitz portfolio optimization problem can be formulated as (M) maximizer subject to xEx 57 e'x = 1 x 0, where e = (1, ...,1) R" and y > 0. Here, r = ('1,...,P.)" ER" where each r; is the expected return on investment i and is the covariance matrix (and so, is positive semidefinite). In practice, the data r is uncertain due to prediction/estimation error. We assume that r belongs to an uncertainty set U given by U = {r R": ||r-1||2

0 is a given constant scalar. The robust optimization approach then aims at finding the worst case solution of problem (M), that is, solving the following robust optimization problem (RM) maximize min{r"x:r U} subject to ex=1 x > 0 xTex 0. Here, r = ('1,...,P.)" ER" where each r; is the expected return on investment i and is the covariance matrix (and so, is positive semidefinite). In practice, the data r is uncertain due to prediction/estimation error. We assume that r belongs to an uncertainty set U given by U = {r R": ||r-1||2

0 is a given constant scalar. The robust optimization approach then aims at finding the worst case solution of problem (M), that is, solving the following robust optimization problem (RM) maximize min{r"x:r U} subject to ex=1 x > 0 xTex

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts