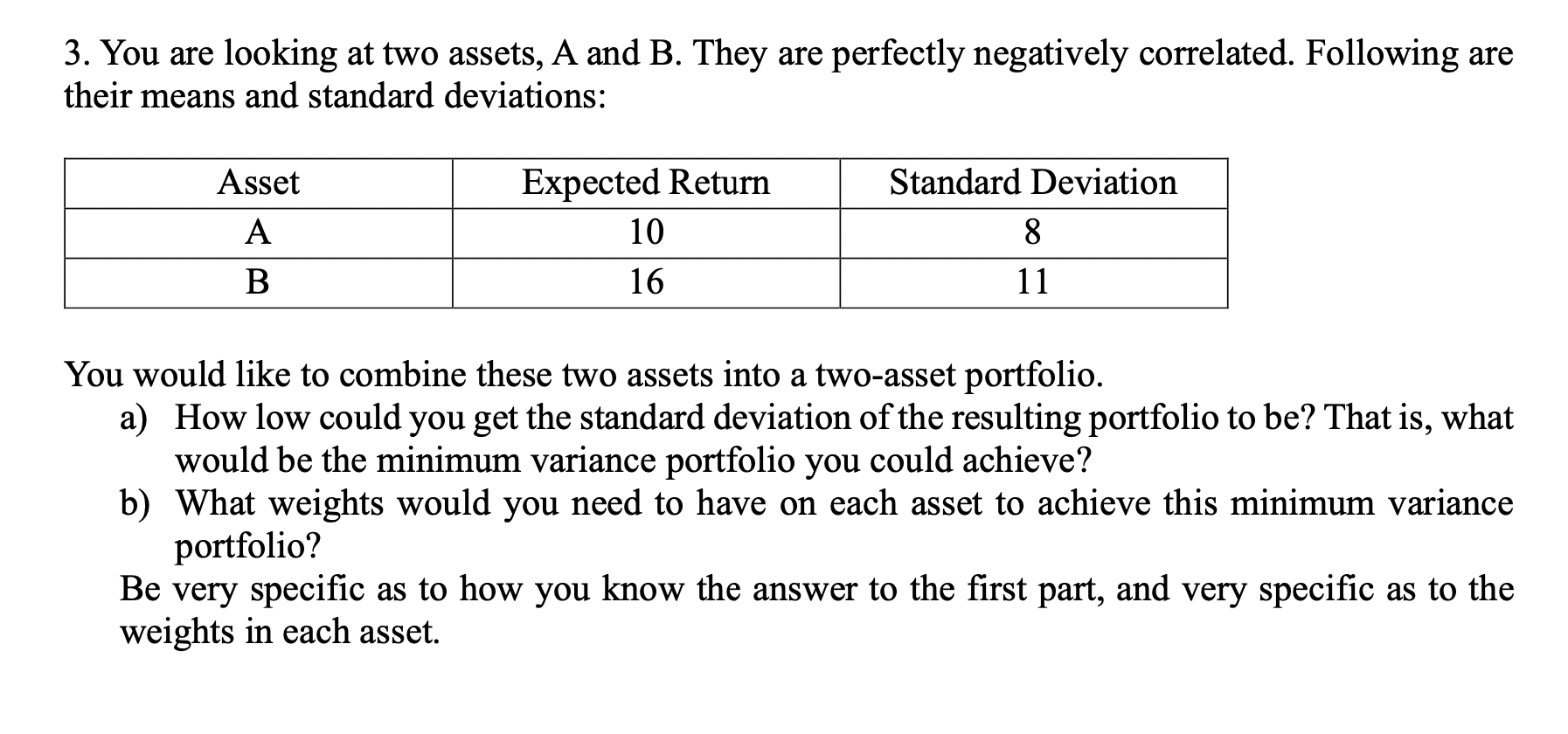

Question: 3. You are looking at two assets, A and B. They are perfectly negatively correlated. Following are their means and standard deviations: Asset A

3. You are looking at two assets, A and B. They are perfectly negatively correlated. Following are their means and standard deviations: Asset A B Expected Return 10 Standard Deviation 8 16 11 You would like to combine these two assets into a two-asset portfolio. a) How low could you get the standard deviation of the resulting portfolio to be? That is, what would be the minimum variance portfolio you could achieve? b) What weights would you need to have on each asset to achieve this minimum variance portfolio? Be very specific as to how you know the answer to the first part, and very specific as to the weights in each asset.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts