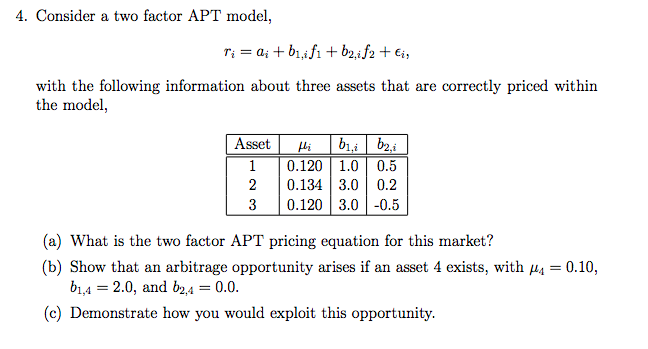

Question: 4. Consider a two factor APT model, with the following information about three assets that are correctly priced within the model, 1 0.1201.0 0.5 2

4. Consider a two factor APT model, with the following information about three assets that are correctly priced within the model, 1 0.1201.0 0.5 2 0.134 3.0 0.2 3 0.120 3.0 -0.5 (a) What is the two factor APT pricing equation for this market? (b) Show that an arbitrage opportunity arises if an asset 4 exists, with H 0.10, b1,4 -2.0, and b24 0.0 (c) Demonstrate how you would exploit this opportunity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock