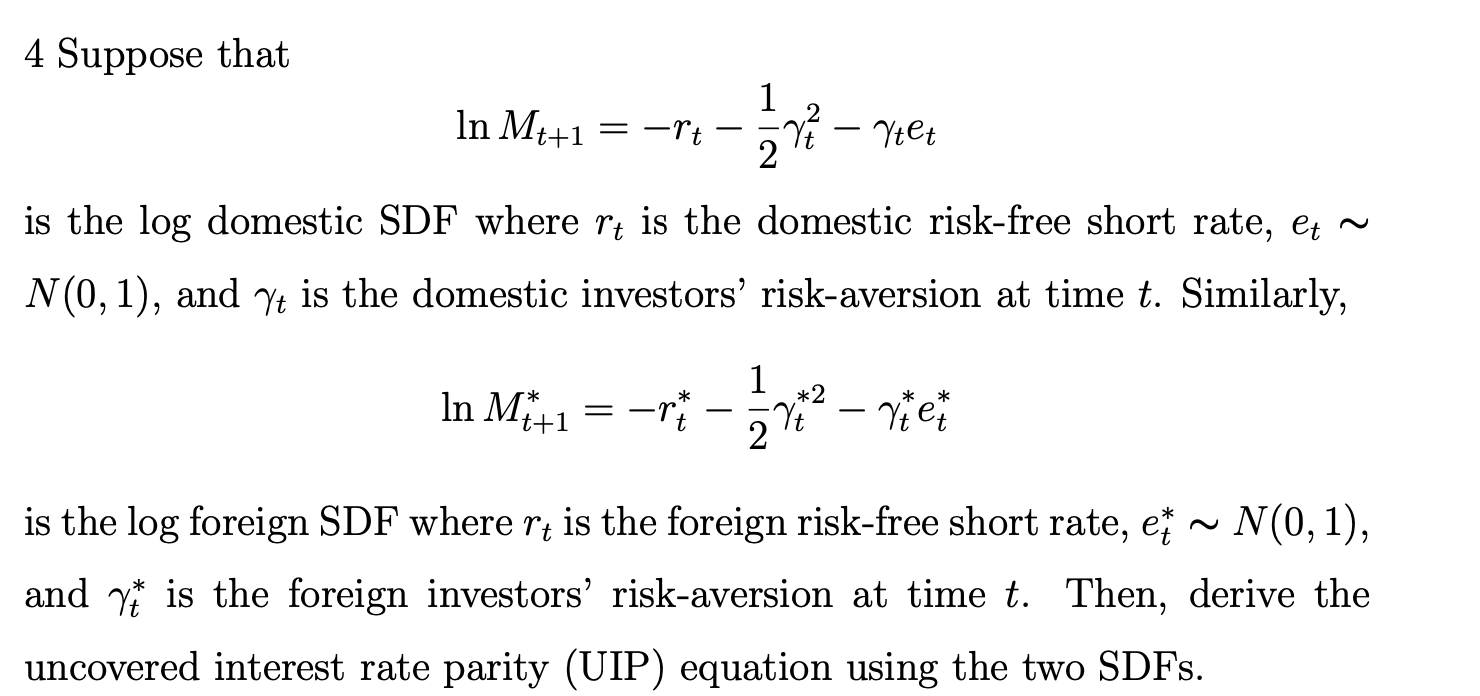

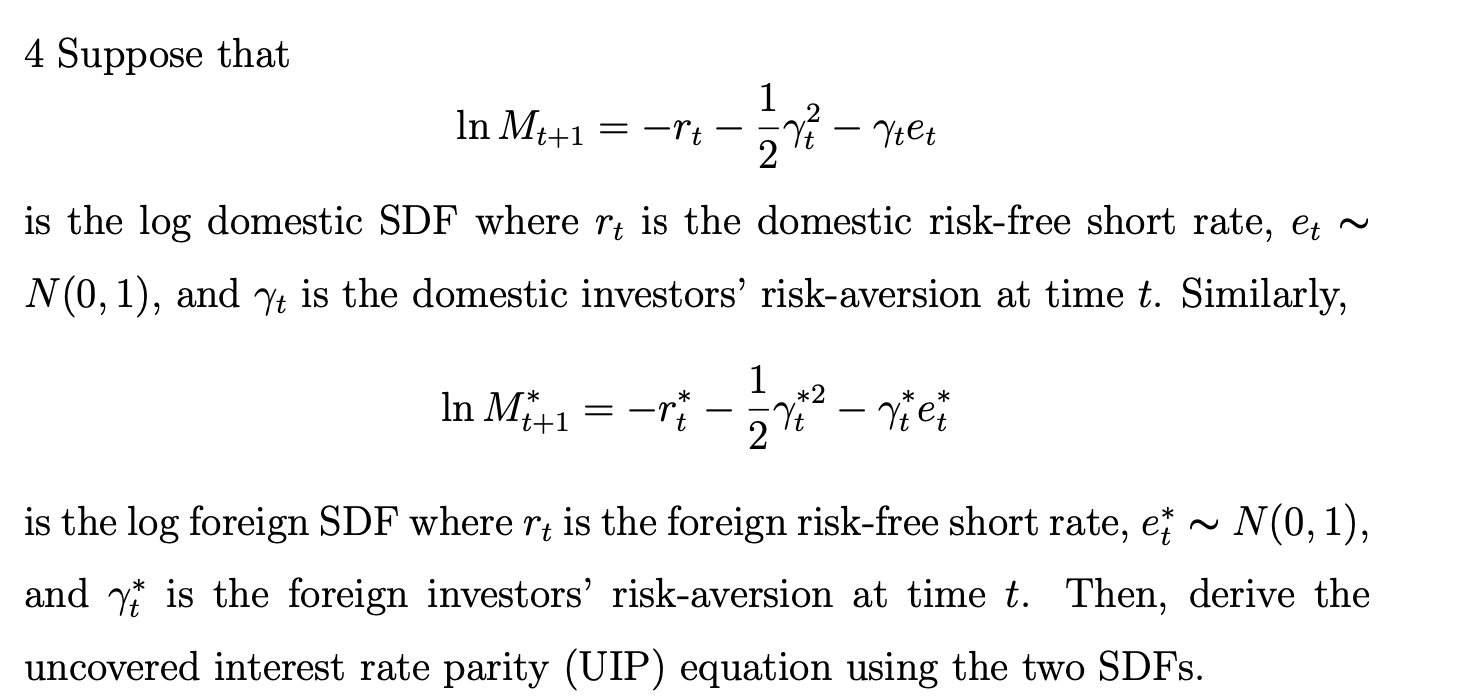

Question: 4 Suppose that In Mt+1 = -rt - 2 It - Vtet is the log domestic SDF where rt is the domestic risk-free short rate,

4 Suppose that In Mt+1 = -rt - 2 It - Vtet is the log domestic SDF where rt is the domestic risk-free short rate, et ~ N(0, 1), and It is the domestic investors' risk-aversion at time t. Similarly, H In M++1 = NO is the log foreign SDF where rt is the foreign risk-free short rate, et ~ N(0, 1), and y is the foreign investors' risk-aversion at time t. Then, derive the uncovered interest rate parity (UIP) equation using the two SDFs

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock