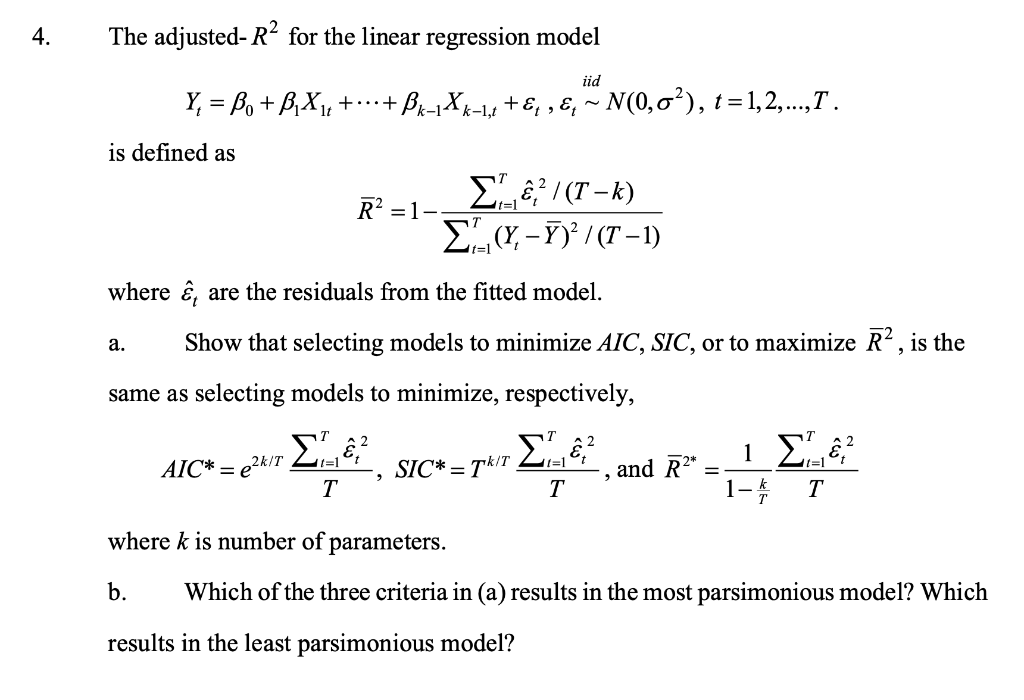

Question: 4. The adjusted-R2 for the linear regression model iid t=1 t=1 Y, = Be + B,X1, +...+Bx-1X61, +E, &, ~ N(0,0%), t=1,2,...,T. is defined as

4. The adjusted-R2 for the linear regression model iid t=1 t=1 Y, = Be + B,X1, +...+Bx-1X61, +E, &, ~ N(0,0%), t=1,2,...,T. is defined as R? =1- -? / (T k) (Y-Y) / (T-1) where , are the residuals from the fitted model. Show that selecting models to minimize AIC, SIC, or to maximize R, is the same as selecting models to minimize, respectively, 1 and R T T 1- T a. AIC* = c24/7 Live? SIC* = tkr E2 = where k is number of parameters. b. Which of the three criteria in (a) results in the most parsimonious model? Which results in the least parsimonious model? 4. The adjusted-R2 for the linear regression model iid t=1 t=1 Y, = Be + B,X1, +...+Bx-1X61, +E, &, ~ N(0,0%), t=1,2,...,T. is defined as R? =1- -? / (T k) (Y-Y) / (T-1) where , are the residuals from the fitted model. Show that selecting models to minimize AIC, SIC, or to maximize R, is the same as selecting models to minimize, respectively, 1 and R T T 1- T a. AIC* = c24/7 Live? SIC* = tkr E2 = where k is number of parameters. b. Which of the three criteria in (a) results in the most parsimonious model? Which results in the least parsimonious model

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts