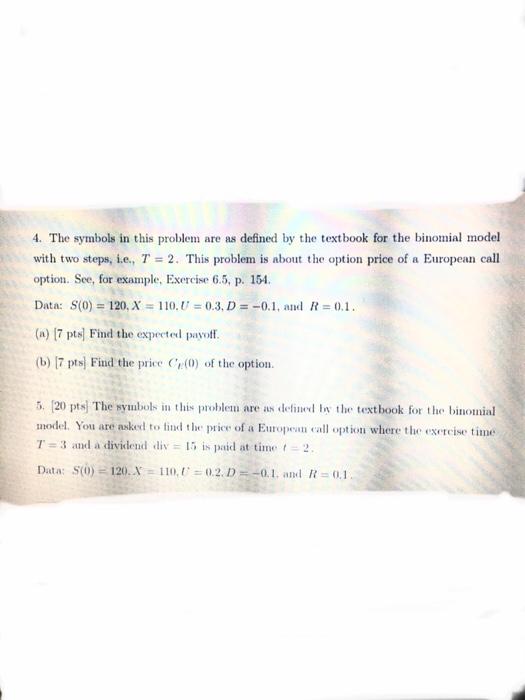

Question: 4. The symbols in this problem are as defined by the textbook for the binomial model with two steps, i.e., T = 2. This problem

4. The symbols in this problem are as defined by the textbook for the binomial model with two steps, i.e., T = 2. This problem is about the option price of a European call option. See, for example, Exercise 6.5, p. 154. Data: S(0) = 120, X = 110. U = 0.3, D = -0.1, and R=0.1. (x) [7 pts) Find the expected pavofl. (b) 17 pts) Find the price () of the option. 5. (20 pts) The symbols in this problem are as defined by the textbook for the binomial model. You are asked to find the price of a Europeut call option where the exercise time T=3 and a dividend vliv = 15 is paid at time = 2 Data: S(O) = 120. X = 110,0 = 0.2.D = -0.1 and R-01

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock