Question: 40 .35 34.1% 34.1% Probability .30 .25 .20 .15 .10 .05 .00 13.6% 13.6% 2.1% 2.15 0.2% 0.2% -4 -2. -1 0 1 2 3

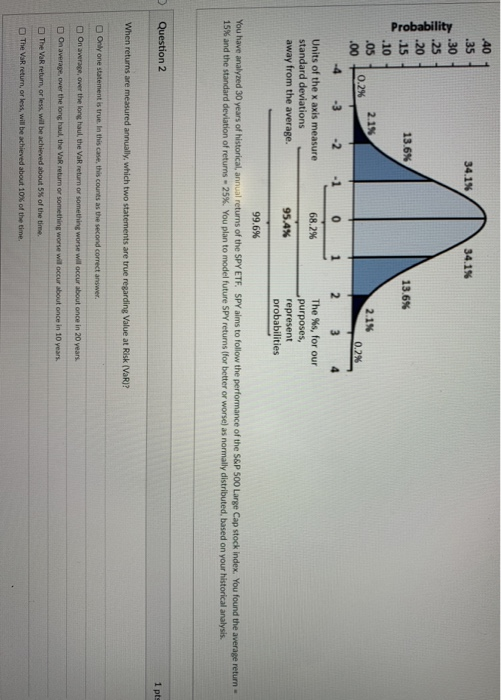

40 .35 34.1% 34.1% Probability .30 .25 .20 .15 .10 .05 .00 13.6% 13.6% 2.1% 2.15 0.2% 0.2% -4 -2. -1 0 1 2 3 68.2% Units of the x axis measure standard deviations away from the average. The is, for our purposes, represent probabilities 95.4% 99.6% You have analyzed 30 years of historical, annual returns of the SPY ETE SPY aims to follow the performance of the S&P 500 Large Cap stock index. You found the average return 15% and the standard deviation of returns -25%. You plan to model future SPY returns (for better or worse) as normally distributed, based on your historical analysis. Question 2 1 pts When returns are measured annually, which two statements are true regarding Value at Risk (VR)? Only one statement is true. In this case, this counts as the second correct answer. On average over the long haul, the VaR return or something worse will occur about once in 20 years. On average over the long haul, the VaRretum or something worse will occur about once in 10 years, The VaR retum, or less will be achieved about 5% of the time The VaR return, or less, will be achieved about 10% of the time

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts