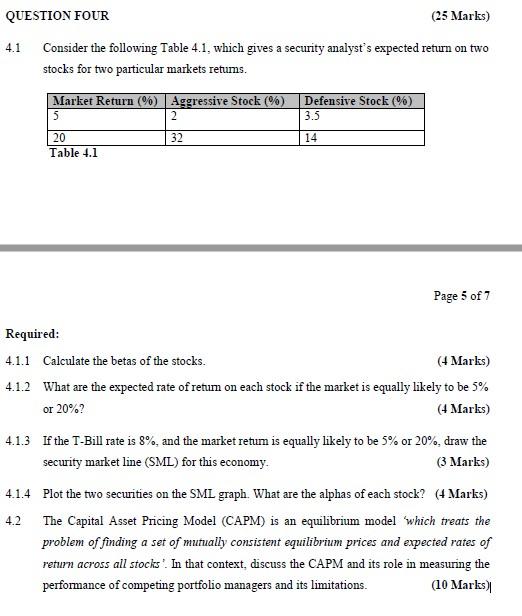

Question: 4.1 Consider the following Table 4.1, which gives a security analyst's expected return on two stocks for two particular markets returns. Required: 4.1.1 Calculate the

4.1 Consider the following Table 4.1, which gives a security analyst's expected return on two stocks for two particular markets returns. Required: 4.1.1 Calculate the betas of the stocks. (4 Marks) 4.1.2 What are the expected rate of return on each stock if the market is equally likely to be 5% or 20% ? (4 Marks) 4.1.3 If the T-Bill rate is 8%, and the market retum is equally likely to be 5% or 20%, draw the security market line (SML) for this economy. (3 Marks) 4.1.4 Plot the two securities on the SML graph. What are the alphas of each stock? (4 Marks) 4.2 The Capital Asset Pricing Model (CAPM) is an equilibrium model 'which treats the problem of finding a set of mutually consistent equilibrium prices and expected rates of return across all stocks'. In that context, discuss the CAPM and its role in measuring the performance of competing portfolio managers and its limitations. (10 Marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts