Question: 5. (15 points) This question involves a simple example that illustrates why o can be estimated by when we compute the heteroskedasticity robust standard

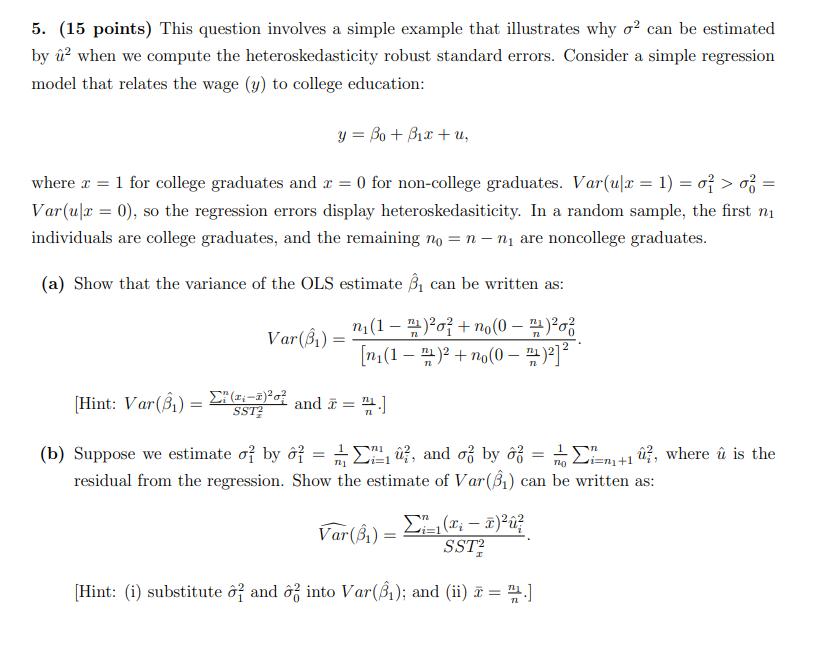

5. (15 points) This question involves a simple example that illustrates why o can be estimated by when we compute the heteroskedasticity robust standard errors. Consider a simple regression model that relates the wage (y) to college education: y = Bo + Bix+u, where x = 1 for college graduates and r = 0 for non-college graduates. Var (ulx = 1) = 0 > 2 = Var(ulx = 0), so the regression errors display heteroskedasiticity. In a random sample, the first ni individuals are college graduates, and the remaining non - n are noncollege graduates. (a) Show that the variance of the OLS estimate 3 can be written as: Var (3) = n(1)o+no(0-24) 02 [n(1)+no(0)] 721 [Hint: Var (3) = (3-7)0 and 2 = 14.] SST? - (b) Suppose we estimate o? by o? =u?, and o? by o = 1/ Ei=+1, where is the residual from the regression. Show the estimate of Var (3) can be written as: Var (3)= = 1(x - x) SST2 [Hint: (i) substitute 2 and o into Var(); and (ii) = 1

Step by Step Solution

There are 3 Steps involved in it

a The variance of the OLS estimate can be written as Var 1 n0 n1 n0 1 n b Suppose we ... View full answer

Get step-by-step solutions from verified subject matter experts