#5- CH 10/11 TANGIBLE ASSETS AND ADJUSTMENTS You are engaged in the examination of the financial...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

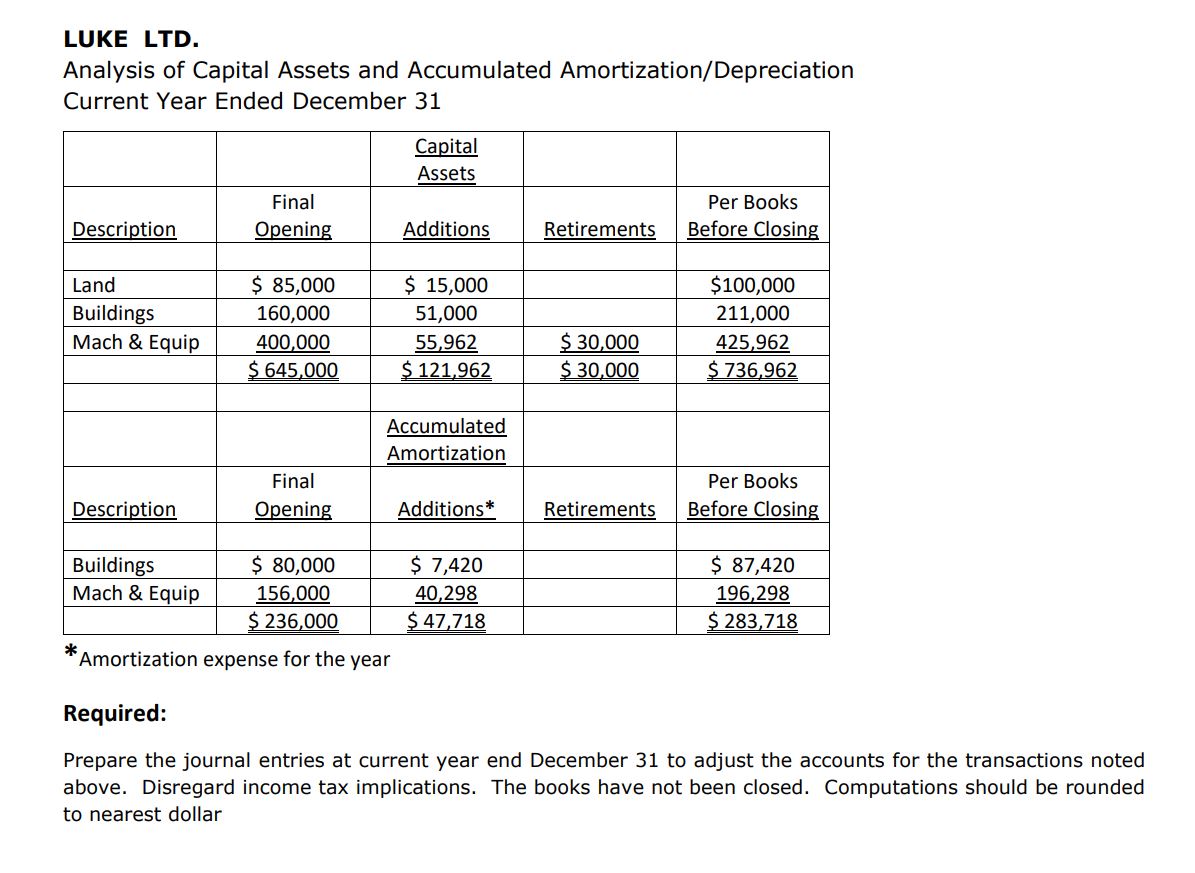

#5- CH 10/11 TANGIBLE ASSETS AND ADJUSTMENTS You are engaged in the examination of the financial statements for Luke Ltd for the current year ended December 31. The analysis that follows for tangible capital assets and related accumulated amortization was prepared by the client. You have verified the opening balances to your prior year's working paper file. Your examination reveals the following information: 1. All plant and equipment were depreciated on the straight-line basis (no residual value taken into consideration) using the following estimated lives: buildings, 25 years; all other items, 10 years. The company's policy was to take one-half year's depreciation on all asset acquisitions and disposals during the year. 2. On April 1, the company entered into a 10-year lease contract for a die-casting machine with annual rentals of $8,000 payable in advance every April 1. The lease could be cancelled by either party (60 days written notice is required) and there was no option to renew the lease or buy the equipment at the end of the lease. The estimated useful life of the machine was 10 years with no residual value. The company recorded the die casting machine in the Machine and Equipment account at $55,962, the present discounted value at the date of lease, and $2,798, applicable to the machine, was included in amortization expense for the year. (Hint: Leases with these conditions should not be capitalized nor should a liability be recognized.) 3. The company completed the construction of a wing on the plant building on June 30 of the current year. The useful life of the building was not extended by this addition. The lowest construction bid received was $51,000, the amount recorded in the Buildings account. Company personnel constructed the addition at a cost of $48,000 (materials, $24,000; labour, $15,000; and overhead, $9,000). The $3,000 difference was credited to an account called Gain on Self-Construction of Building Addition. 4. On August 18, $15,000 was paid for paving and fencing a portion of land owned by the company to be used as a parking lot for the employees. The expenditure was charged to the Land account. 5. The amount shown in the machinery and equipment asset retirement column represents cash received on September 5 regarding disposal of a machine purchased in July 4 years ago, for $60,000. The bookkeeper recorded amortization expense of $4,500 on this machine in the current year. 6. The city of Moose Jaw donated land and a building appraised at $20,000 and $69,000 respectively to Luke Ltd. For a plant. On September 1, the company began operating the plant. Because the company paid nothing for these assets, the bookkeeper made no entry to record the transaction. LUKE LTD. Analysis of Capital Assets and Accumulated Amortization/Depreciation Current Year Ended December 31 Capital Assets Description Final Opening Additions Retirements Per Books Before Closing Land Buildings $ 85,000 160,000 $ 15,000 $100,000 51,000 211,000 Mach & Equip 400,000 $645,000 55,962 $ 121,962 $ 30,000 $30,000 425,962 $736,962 Accumulated Amortization Description Final Opening Additions* Retirements Per Books Before Closing Buildings Mach & Equip $ 80,000 156,000 $ 7,420 40,298 $ 87,420 $236,000 $ 47,718 196,298 $283,718 *Amortization expense for the year Required: Prepare the journal entries at current year end December 31 to adjust the accounts for the transactions noted above. Disregard income tax implications. The books have not been closed. Computations should be rounded to nearest dollar #5- CH 10/11 TANGIBLE ASSETS AND ADJUSTMENTS You are engaged in the examination of the financial statements for Luke Ltd for the current year ended December 31. The analysis that follows for tangible capital assets and related accumulated amortization was prepared by the client. You have verified the opening balances to your prior year's working paper file. Your examination reveals the following information: 1. All plant and equipment were depreciated on the straight-line basis (no residual value taken into consideration) using the following estimated lives: buildings, 25 years; all other items, 10 years. The company's policy was to take one-half year's depreciation on all asset acquisitions and disposals during the year. 2. On April 1, the company entered into a 10-year lease contract for a die-casting machine with annual rentals of $8,000 payable in advance every April 1. The lease could be cancelled by either party (60 days written notice is required) and there was no option to renew the lease or buy the equipment at the end of the lease. The estimated useful life of the machine was 10 years with no residual value. The company recorded the die casting machine in the Machine and Equipment account at $55,962, the present discounted value at the date of lease, and $2,798, applicable to the machine, was included in amortization expense for the year. (Hint: Leases with these conditions should not be capitalized nor should a liability be recognized.) 3. The company completed the construction of a wing on the plant building on June 30 of the current year. The useful life of the building was not extended by this addition. The lowest construction bid received was $51,000, the amount recorded in the Buildings account. Company personnel constructed the addition at a cost of $48,000 (materials, $24,000; labour, $15,000; and overhead, $9,000). The $3,000 difference was credited to an account called Gain on Self-Construction of Building Addition. 4. On August 18, $15,000 was paid for paving and fencing a portion of land owned by the company to be used as a parking lot for the employees. The expenditure was charged to the Land account. 5. The amount shown in the machinery and equipment asset retirement column represents cash received on September 5 regarding disposal of a machine purchased in July 4 years ago, for $60,000. The bookkeeper recorded amortization expense of $4,500 on this machine in the current year. 6. The city of Moose Jaw donated land and a building appraised at $20,000 and $69,000 respectively to Luke Ltd. For a plant. On September 1, the company began operating the plant. Because the company paid nothing for these assets, the bookkeeper made no entry to record the transaction. LUKE LTD. Analysis of Capital Assets and Accumulated Amortization/Depreciation Current Year Ended December 31 Capital Assets Description Final Opening Additions Retirements Per Books Before Closing Land Buildings $ 85,000 160,000 $ 15,000 $100,000 51,000 211,000 Mach & Equip 400,000 $645,000 55,962 $ 121,962 $ 30,000 $30,000 425,962 $736,962 Accumulated Amortization Description Final Opening Additions* Retirements Per Books Before Closing Buildings Mach & Equip $ 80,000 156,000 $ 7,420 40,298 $ 87,420 $236,000 $ 47,718 196,298 $283,718 *Amortization expense for the year Required: Prepare the journal entries at current year end December 31 to adjust the accounts for the transactions noted above. Disregard income tax implications. The books have not been closed. Computations should be rounded to nearest dollar

Expert Answer:

Related Book For

Intermediate Accounting

ISBN: 978-0324300987

10th Edition

Authors: Loren A Nikolai, D. Bazley and Jefferson P. Jones

Posted Date:

Students also viewed these finance questions

-

(a) Using your knowledge of economics and how markets work illustrate and explain why the price of electricity has increased so much over the past 18 months throughout the EU. You should consider the...

-

Elaine's original basis in the Hornbeam Partnership was $30,000. Her share of the taxable income from the partnership since she purchased the interest has been $90,000, and Elaine has received...

-

True or false? Explain: modularity reduces complexity because A. It reduces the effect of incommensurate scaling. B. It helps control propagation of effects.

-

Calculate the following: \(1.14 \times 10^{-43}+2.56 \times 10^{-46}\)

-

The balance sheet for Bukin Corporation follows. Current assets ............. $ 300,000 Long-term assets (net) .......... 950,000 Total assets ............... $1,250,000 Current liabilities...

-

(a) Suppose the current stock price is $25, the strike price is $65, the variance of the stock is 0.4, and the risk-free rate is 0.07. If the option has six months to expiration. (i) ...

-

https://vle.phoenix.edu/ultra/courses/_322731_1/outline/assessment/_31872471_1/overview/attempt/_35331684_1?courseld=_322731_1 Quniversity of phoenix - Search Home View Assessment + BUS/475:...

-

Conley Corp s post - closing trial balance in alphabetical order as of December 3 1 , 2 0 2 3 was as follows: Debit Credit Accounts Payable $ 3 2 0 , 0 0 0 Accounts Receivable $ 4 7 0 , 0 0 0...

-

You are the financial director of Dawn Ltd ( Dawn ) , the parent company of the Dawn group. All companies within the group s reporting date is 3 1 December. Extract of the trial balances as at 3 1...

-

On January 1 , 2 0 2 5 , Sheridan Inc. had these stockholders' equity balances. Common Stock, $ 1 par ( 2 , 7 0 0 , 0 0 0 shares authorized, 6 6 0 , 0 0 0 shares issud and outstnding. Paid - in...

-

CC Corporation provides you with the following information from its accounting records this year related to income and all book - tax differences. Pre - tax book income: $ 3 1 9 , 0 0 0 GAAP warranty...

-

On January1, 20X7, Mannix Corporation purchased 80% of the outstanding common stock of Raun Company. No excess of cost or book value resulted from the acquisition. The following information has been...

-

Marigold Corp. was incorporated on January 2, 2020, but was unable to begin manufacturing activities until July 1, 2020, because new factory facilities were not completed until that date. The Land...

-

The Taylor's series expansion for cosx about x = 0 is given by: where x is in radians. Write a user-defined function that determines cosx using Taylor's series expansion. For function name and...

-

A large company has a standard sales contract, but sales personnel frequently modify the terms of the contract. Sales personnel frequently grant authorized and unrecorded sales discounts to customers...

-

How should auditors search for hidden liabilities?

-

How could auditors have stopped Parmalat's deceptions?

Study smarter with the SolutionInn App