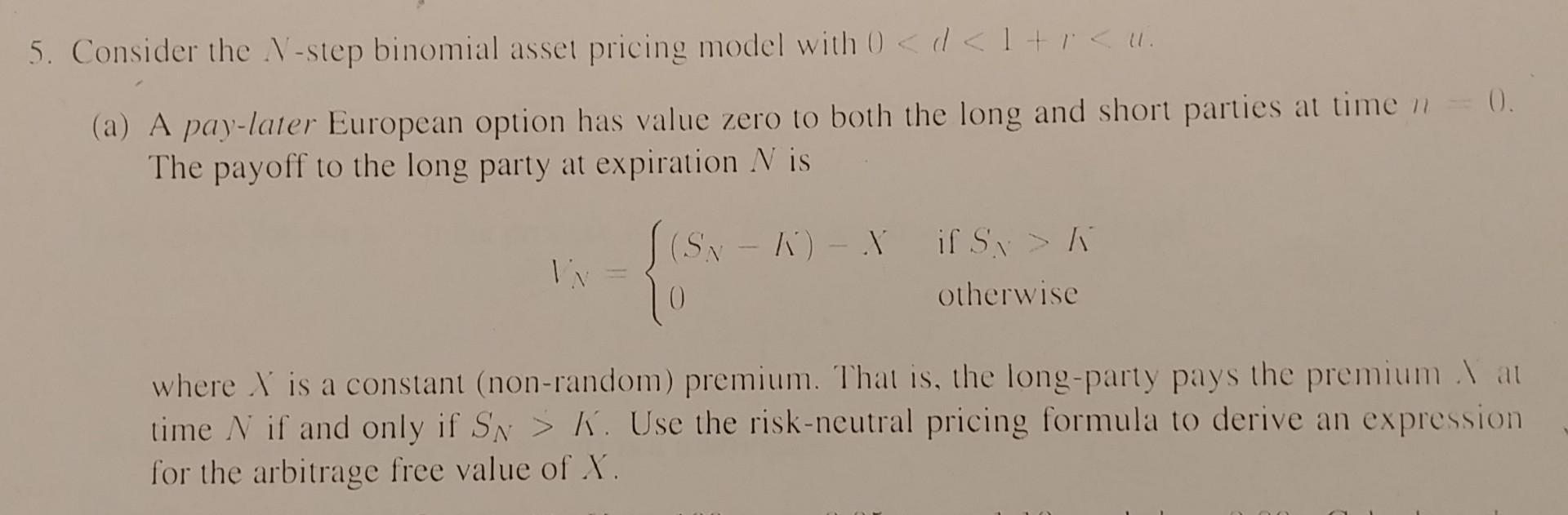

Question: 5. Consider the V-step binomial asset pricing model with 0 k otherwise where I is a constant (non-random) premium. That is, the long-party pays the

5. Consider the V-step binomial asset pricing model with 0 k otherwise where I is a constant (non-random) premium. That is, the long-party pays the premium lat time N if and only if Sn > K. Use the risk-neutral pricing formula to derive an expression for the arbitrage free value of X 5. Consider the V-step binomial asset pricing model with 0 k otherwise where I is a constant (non-random) premium. That is, the long-party pays the premium lat time N if and only if Sn > K. Use the risk-neutral pricing formula to derive an expression for the arbitrage free value of X

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock