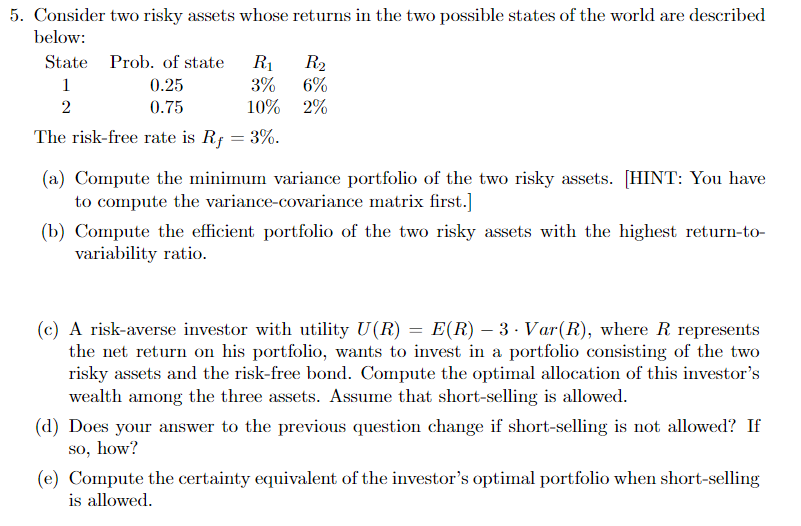

Question: 5. Consider two risky assets whose returns in the two possible states of the world are described below: State Prob. of state R1 R2 1

5. Consider two risky assets whose returns in the two possible states of the world are described below: State Prob. of state R1 R2 1 0.25 3% 6% 0.75 10% 2% The risk-free rate is R = 3%. (a) Compute the minimum variance portfolio of the two risky assets. (HINT: You have to compute the variance-covariance matrix first.] (b) Compute the efficient portfolio of the two risky assets with the highest return-to- variability ratio. (c) A risk-averse investor with utility U(R) = E(R) 3. Var(R), where R represents the net return on his portfolio, wants to invest in a portfolio consisting of the two risky assets and the risk-free bond. Compute the optimal allocation of this investor's wealth among the three assets. Assume that short-selling is allowed. (d) Does your answer to the previous question change if short-selling is not allowed? If so, how? (e) Compute the certainty equivalent of the investor's optimal portfolio when short-selling is allowed. 5. Consider two risky assets whose returns in the two possible states of the world are described below: State Prob. of state R1 R2 1 0.25 3% 6% 0.75 10% 2% The risk-free rate is R = 3%. (a) Compute the minimum variance portfolio of the two risky assets. (HINT: You have to compute the variance-covariance matrix first.] (b) Compute the efficient portfolio of the two risky assets with the highest return-to- variability ratio. (c) A risk-averse investor with utility U(R) = E(R) 3. Var(R), where R represents the net return on his portfolio, wants to invest in a portfolio consisting of the two risky assets and the risk-free bond. Compute the optimal allocation of this investor's wealth among the three assets. Assume that short-selling is allowed. (d) Does your answer to the previous question change if short-selling is not allowed? If so, how? (e) Compute the certainty equivalent of the investor's optimal portfolio when short-selling is allowed

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts