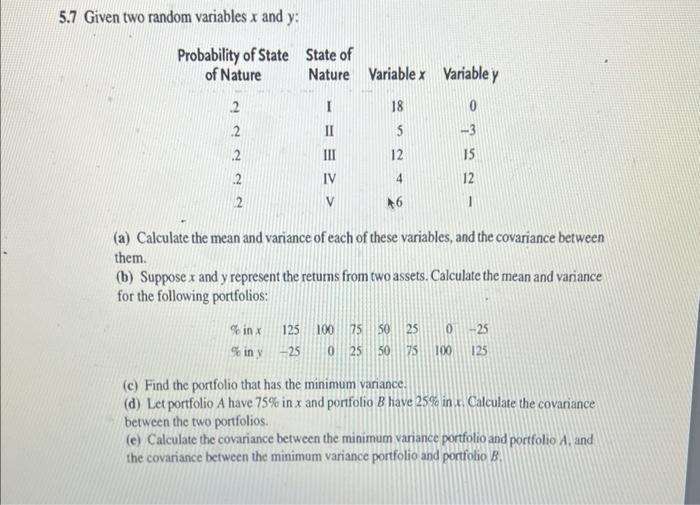

Question: 5.7 Given two random variables x and y : (a) Calculate the mean and variance of each of these variables, and the covariance between them.

5.7 Given two random variables x and y : (a) Calculate the mean and variance of each of these variables, and the covariance between them. (b) Suppose x and y represent the retums from two assets. Calculate the mean and variance for the following portfolios: (c) Find the portfolio that has the minimum variance. (d) Let portfolio A have 75% in x and portfolio B have 25% in x. Calculate the covariance between the two portfolios. (e) Calculate the covariance between the minimum variance portfolio and portfolio A, and the covariance between the minimum variance portfolio and portfolio B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock