Question: 6. (20pts) Consider two risky assets A and B. Your forecasts for their expected return and standard deviation are presented in the following table. You

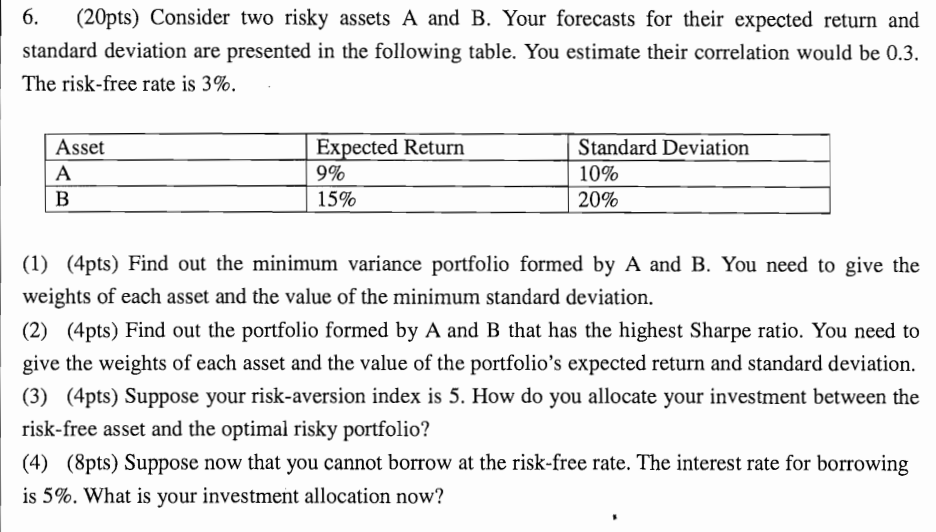

6. (20pts) Consider two risky assets A and B. Your forecasts for their expected return and standard deviation are presented in the following table. You estimate their correlation would be 0.3. The risk-free rate is 3%. (1) (4pts) Find out the minimum variance portfolio formed by A and B. You need to give the weights of each asset and the value of the minimum standard deviation. (2) (4pts) Find out the portfolio formed by A and B that has the highest Sharpe ratio. You need to give the weights of each asset and the value of the portfolio's expected return and standard deviation. (3) (4pts) Suppose your risk-aversion index is 5. How do you allocate your investment between the risk-free asset and the optimal risky portfolio? (4) (8pts) Suppose now that you cannot borrow at the risk-free rate. The interest rate for borrowing is 5%. What is your investment allocation now? 6. (20pts) Consider two risky assets A and B. Your forecasts for their expected return and standard deviation are presented in the following table. You estimate their correlation would be 0.3. The risk-free rate is 3%. (1) (4pts) Find out the minimum variance portfolio formed by A and B. You need to give the weights of each asset and the value of the minimum standard deviation. (2) (4pts) Find out the portfolio formed by A and B that has the highest Sharpe ratio. You need to give the weights of each asset and the value of the portfolio's expected return and standard deviation. (3) (4pts) Suppose your risk-aversion index is 5. How do you allocate your investment between the risk-free asset and the optimal risky portfolio? (4) (8pts) Suppose now that you cannot borrow at the risk-free rate. The interest rate for borrowing is 5%. What is your investment allocation now

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts